The Long Cycle in Australian Construction Productivity

Over the last 15 years, Construction productivity in Australia has gone through a long cycle and ended up more or less where it began. The Australian Bureau of Statistics Construction labour productivity index rose from 92.88 in 2006-07 to 95.36 in 2010-11, before rapidly increasing to 115.94 in 2013-14, then falling to 99.1 in 2021-22. What explains the 10 year cycle between 2011 and 2021?

Productivity estimates require both a measure of labour inputs, such as hours worked or people employed, and a measure of output, called Industry value added (IVA, the difference between total revenue and total costs). IVA is then adjusted for changes in prices of materials and labour to estimate Gross value added (GVA) using price indexes. The ABS has a Construction industry labour productivity index, but does not have separate indexes for the different construction industry sectors.

However, using GVA data, estimates of productivity for the industry sectors of Engineering construction, Building construction and Construction services can be found. The GVA data comes from the ABS National Accounts (chain volume measures of economic activity). The number of people employed includes all workers in June each year, and comes from ABS Australian Industry. The construction work done data is from the ABS chain volume Value of Construction Work Done, which is expenditure on construction adjusted for inflation.

GVA per person employed is a useful proxy for industry productivity. As a combination of real output and employment, GVA per person employed looks like a measure of productivity and, while not precise, it is indicative of industry trends. As a measure of productivity, annual GVA per person employed follows a similar path to the ABS productivity index, which uses the number of hours worked for labour input. If output is increasing faster than employment, labour productivity will also increase.

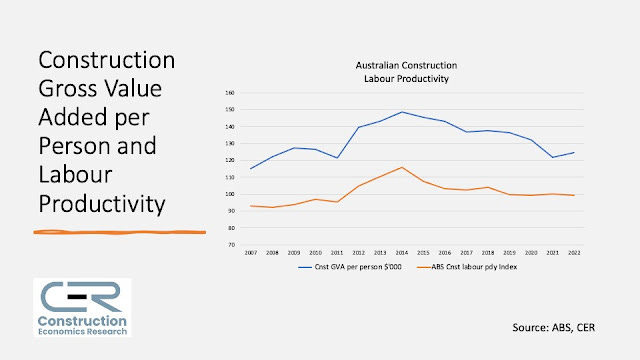

In Figure 1 Construction GVA per person employed in thousands of dollars per person is compared to the ABS labour productivity index for Construction from their Estimates of Industry Multifactor Productivity. There is a good match between the two because they both use industry GVA for output and are both based on the 2020-21 year, although the long cycle between 2011 and 2021 is more pronounced in the GVA per person data. The ABS labour productivity index is 2020-21 = 100, and went from 92.88 in 2006-07 to 115.94 in 2013-14 before falling to 99.1 in 2021-22.

Figure 1. Construction Gross Value Added per Person Employed and Labour Productivity

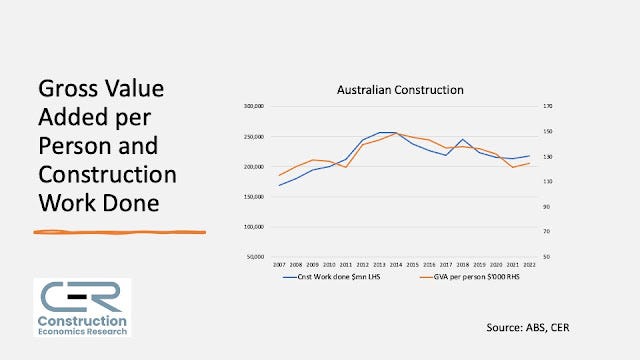

In Figure 2 the Value of construction work done is shown with GVA per person employed, and there is a clear relationship between the two. Over the 15 year period Construction work done peaked twice, first in 2014 during the mining boom and then in 2018 with new infrastructure projects. Construction GVA per person followed a similar trend to the rises and falls in work done.

Figure 2. Gross Value Added per Person Employed and Construction Work Done

Significantly, Figure 2 shows GVA per person employed also peaked in 2014 as it followed changes in work done. Productivity increased when construction was rising after 2011 during the mining boom, and then decreased as the mining boom ended. The first stage of this long-run cycle of increasing construction work done and GVA per person employed in construction was entirely due to the large number of large, capital intensive resource projects completed during the mining boom between 2011 and 2017, followed by transport and energy sectors commencing in the second stage from 2018.

Engineering Construction

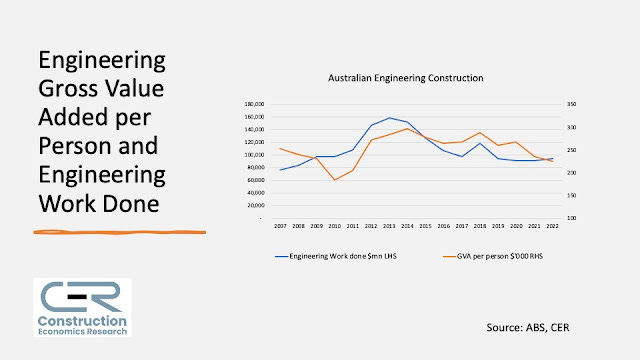

The mining boom started in the 2000s but took off after 2010 with many large energy and resource projects. As Figure 3 shows, the value of Engineering work done doubled between 2007 and 2013, and as it did Engineering GVA per person employed increased by around 20%. Engineering GVA per person followed the rise and fall and subsequent fall in the value of work done, and is now well below the peak years. The value of Engineering work done includes associated expenditure on machinery and equipment, so a lot of the increase was due to the capital investment required for the LNG plants, offshore platforms, railways and new mines constructed.

Figure 3. Gross Value Added per Person Employed and Engineering Work Done

Building Construction and Construction Services

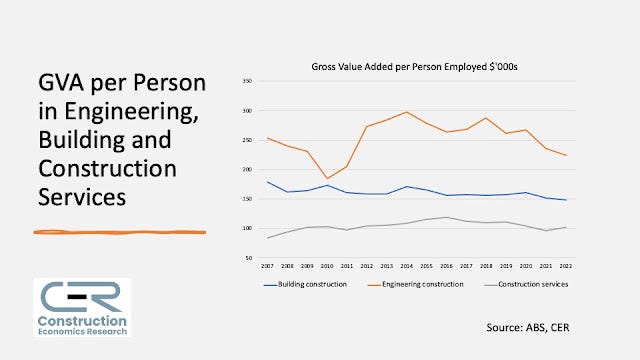

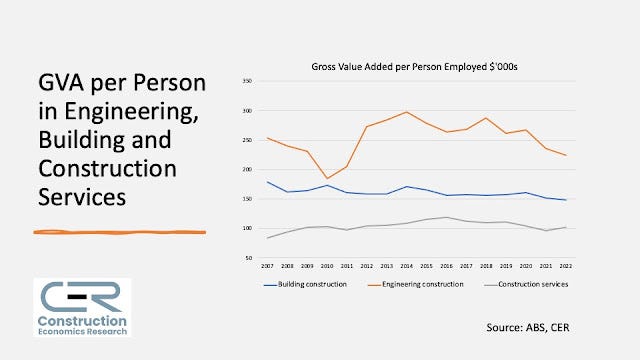

Using Australian Industry employment data, GVA per person employed can also be found for both Building construction and Construction services as well as Engineering. Here a slight decline in Building has been offset by a small rise in Construction services GVA per person over the 15 years, as GVA per person since 2006-07 in Building has declined slightly, from $179,000 to $148,000 in 2021-22, while it increased for Construction services, from $84,000 to $102,000. As shown in Figure 4, the level of GVA per person in Construction services is around two-thirds of the level for Building construction, because Construction services are generally labour intensive and will therefore have a lower value of output per person.

The range in output per person employed between Engineering, Building and Construction services reflects the differences in capital requirements of these three sectors, and expenditure on purchases of software, equipment and machinery by firms in the three sectors. The higher the capital requirements, or capital intensity, of an industry, the higher the level of output per person employed is expected to be, because workers with more capital are more productive. Both excavators and shovels require one operator, but the former shifts more soil.

Figure 4. GVA per Person Employed in Engineering, Building and Construction Services

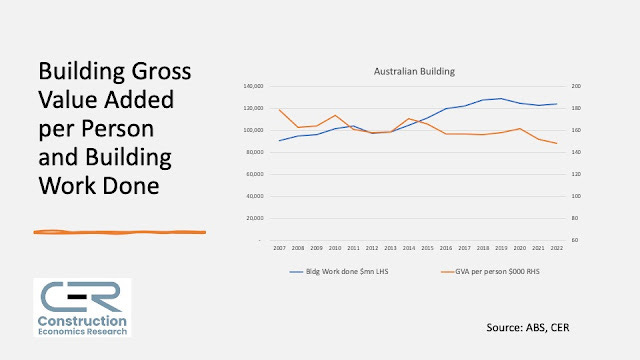

The strong relationship between the value of Engineering work done and GVA per person seen in Engineering is not found for Building and the value of Building work done. Despite the increase in the value of Building work done after 2014 there was no increase in GVA per person, rather there was a slight decline as residential building increased during the transition after the mining boom, as shown in Figure 5. This may also be an indicator of increased use of prefabrication and offsite manufacturing reducing the value added of onsite work, but we have no reliable data on that.

Figure 5. Gross Value Added per Person Employed and Building Work Done

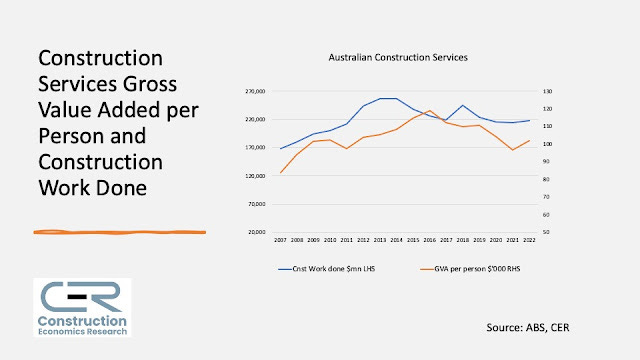

For Construction Services there is real GVA but not real work done data, so total construction work done is used in Figure 6, as the trades work across Building and Engineering. Here, GVA per person does increase as work increases, but peaks in 2016 and then falls away. The number of people employed increased from 723,000 in 2015-16 to 854,000 in 2020-21, and may have contributed to the fall in GVA per person if that increase included many new workers with little experience and limited skills. There was a particularly big increase in employment in 2020-21, when over 60,000 more people were employed in Construction services, and employment grew much faster than work done. As a result, GVA per person dropped by $8,000 before recovering in 2021-22.

Figure 6. Gross Value Added per Person Employed and Total Construction Work Done

Conclusion

Over the last 15 years, construction productivity in Australia has gone through a long cycle and ended up more or less where it began. Rising from $115,000 per person employed in 2007 to $149,000 in 2014, an increase of 29%, GVA per person employed then started falling and was back to $125,000 per person in 2022.

This long cycle in Australian construction productivity followed changes in the value of Engineering work done. Productivity increased as Engineering construction rose after 2011, and then decreased as the mining boom ended. This long-run cycle in construction productivity was entirely due to the capital intensive resource projects completed between 2011 and 2017 by Engineering construction, where the machinery and equipment required for LNG plants, offshore platforms and new mines is included in the value of work done. This greatly increased the value of work done, but much of the increase was therefore not invested directly in construction work.

The strong relationship between changes in the value of work done and GVA per person seen in Engineering is not found for Building construction or Construction services. The higher capital intensity of Engineering work appears to lift GVA per person with increasing work done, as more expenditure on machinery and equipment is included in this sector compared to building.

Despite the increase in the value of building work done after 2014 there was no increase in Building GVA per person, rather there was a slight decline. For Construction services, GVA per person did increase to 2016 as construction work done increased, before falling away as the number of people employed increased faster than the value of work done.

What can be taken from this episode? Firstly, over 15 years there has been little change in overall construction labour productivity and, unlike Engineering, for Building and Construction services increasing work done has seen productivity fall slightly since 2014 as employment increased faster than output. Second, the lack of any real trend in construction productivity, despite changes in output and a continual increase in the number of people employed, suggests the industry is at the limits of efficiency, based on current technology. As output increases the number of people also increases, often a bit more than output but sometimes slightly less, so GVA per person is not improving. Therefore the industry may be somewhere close to the efficiency frontier in delivering projects, but there is no trend at either the industry or sector level of increasing productivity.