The HomeBuilder Program and Australian Housing

State and federal governments criticised in COVID inquiry report

The release of the COVID 19 Response Inquiry Report on October 28th included a section on the HomeBuilder program. This was the third report on HomeBuilder, following a KPMG report on the National Partnership Agreement in 2022 and an AHURI report on Responding to the Pandemic in 2020. There was also a review by PWC for Treasury in 2020.

A book published in 1979 called The Construction Industry: Balance Wheel of the Economy argued counter-cyclical economic policy increased construction during recessions, through expenditure on public projects and the effect on residential building of lower interest rates. This has often been the case, in Australia the Rudd Government increased public expenditure on construction after the 2008 financial crisis and the Reserve Bank lowered interest rates to boost residential work after the mining boom ended in 2014.

From this perspective, HomeBuilder was a conventional policy, introduced to counter the recessionary effects of the COVID-19 pandemic. In 2020 economic activity was decreasing and there were estimates of potential GDP losses of up to 20%. In a 2022 speech the Treasury Secretary Steven Kennedy said: ‘The pandemic was unlike any other downturn in recent history and precipitated the most severe economic downturn since the Great Depression. It was a health crisis before it became an economic crisis. Public health restrictions and cautious behaviour by people who didn’t want to catch the virus severely disrupted daily life and led to a sharp decline in output.’

Total Australian Government spending on economic support measures was $314 billion, or 15.2% of GDP. In that context, HomeBuilder was a minor program compared to the tens of billions spent on JobKeeper and other transfer payments. However, those were programs administered by the Australian Tax office for a large proportion of the population, whereas HomeBuilder was a targeted program administered by the states and territories with strict eligibility requirements.

This post first outlines the program, followed by the relevant section of the Inquiry report, and the review of the National Partnership Agreement. It assesses the effectiveness and consequences of HomeBuilder. How accurate were the forecasts of expenditure on the program? What were the goals of the program and were they achieved? What were the outcomes? Is it an example of good policy, or of poor policy-making that did not consider industry characteristics and capacity?

Outline of the HomeBuilder Program

The program was introduced in mid-2020 to support residential construction by providing a grant of $25,000. Applicants had to have signed contracts between 4 June 2020 and 31 December 2020 to purchase a house and land package, build a new home, do a substantial rebuild or renovation of an owner-occupied property, or purchase an off-plan apartment or townhouse. Construction had to have commenced within three months of the contract date. On 29 November the program was extended to 31 March 2021, with the grant reduced to $15,000 and the commencement time increased to six months. In April 2021 the construction commencement time was increased to 18 months.

There was an eligibility income cap of $125,000 for an individual or $200,000 for a couple, based on 2018-19 or later taxable income (the lack of clarity here became a source of confusion and an issue for the states and territories). There was also a cap on the value of new builds that differed between states, and on the value of renovations. However, the grant amount was the same everywhere for everyone, and the program itself was uncapped.

The government underestimated take-up of the program. It was forecast to support 27,132 applications totalling $680 million, with the extension expected to add 15,000 applications at an estimated cost of $241 million. However, by June 2024 113,156 applications had been approved and $2.6 billion had been paid. Although applications closed in April 2021, there may be further costs as applicants have until 30 June 2025 to submit documents supporting their applications.

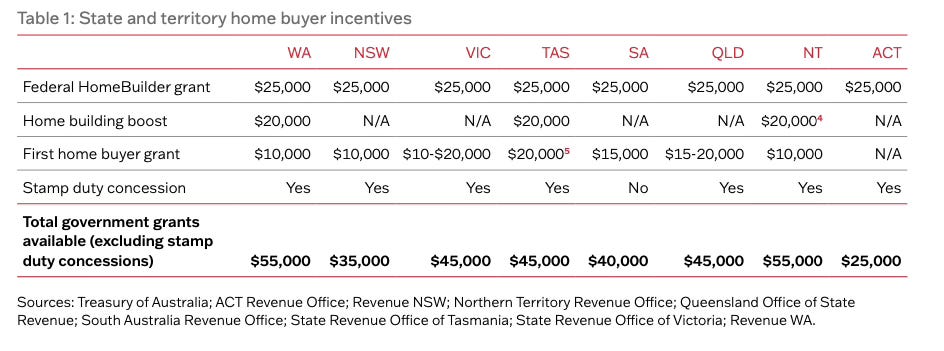

HomeBuilder was implemented through a National Partnership Agreement with the state and territory governments, which made the states responsible for administering the program. It was designed to complement existing state and territory First Home Owner Grants Programs, then all states except South Australia gave stamp duty concessions for new builds (whose value varied greatly but might be up to $40,000 depending on the house and location), and Western Australia, Tasmania and the Northern Territory added an extra ‘home building boost’. Combining HomeBuilder with the state and territory schemes, first home buyers in Western Australia and the Northern Territory could access $55,000 in grants, in Queensland, Victoria and Tasmania up to $45,000 in grants, and in NSW $35,000. The federal and state programs are in Table 1.

Source: AHURI 2020: 15. Responding to the Pandemic. The table does not include the value of stamp duty exemptions.

The COVID Inquiry Report

The report included a couple of interesting data points on construction during COVID. It noted industries with a large proportion of small businesses received most of the JobKeeper and Cash Flow Boost payments, including construction, which received $2.5 billion. These payments were made to employers. There was also a graph of changes to revenue for firms between 2019 and 2020 (p. 582), which showed 45% of construction firms increased their revenue, 30% had decreased revenue by up to 50%, and there were 15% of firms with revenue decreasing by more than 50%.

The report focused on the inflationary effects of HomeBuilder. Between September 2021 and September 2022 the contribution of housing to quarterly inflation was between 20% and 40% of the total change in the consumer price index (CPI). The fiscal stimulus from government grants combined with existing labour shortages, exacerbated by border closures, and pandemic related supply chain disruptions that increased material costs. As a result, the cost of building a house increased by around 30% during COVID.

Table 2. Construction contribution to quarterly inflation (% change)

Sep 21 Dec 21 Mar 22 Jun 22 Sep 22

Construction 0.35 0.37 0.56 0.52 0.67

Total CPI 0.8 1.3 2.1 1.8 1.8

Source: COVID 19 Response Inquiry Report 2024: 59. From ABS data.

The inquiry report found the program inappropriate and inflationary: ‘the HomeBuilder program created excess demand in an industry facing supply constraints. This has been a significant contributor to inflation coming out of the pandemic, and the program’s focus on renovations rather than new builds added to the general housing shortages. These types of demand-side stimulus measures are largely not appropriate in pandemics where industries are facing supply constraints’ (p. 549).

A counter-cyclical increase of government expenditure in a recession is a common use of fiscal policy, and the construction industry is often targeted because it is both an employer of many workers and a major source of demand for domestic suppliers. The inquiry report concluded: ‘There are clear indications that the infrastructure measures taken – in particular, HomeBuilder – overheated the industry and contributed to inflation in the post-pandemic era. The program was designed explicitly to stimulate aggregate demand and support the residential construction sector. It acted to stimulate consumption expenditure and lowered the significant household savings built up during the pandemic. However, the measure failed to appropriately take into account the supply-side effects of the pandemic’ (p. 593)

The section of the Inquiry report on HomeBuilder is unsatisfactory because, apart from the 113,156 applications received and the table on CPI, there is no other data. A review of the program that does not include houses commenced and completed, or people employed, is not comprehensive and does not allow conclusions to be drawn on the effectiveness of the program. That data is provided below when assessing the program.

In an immediate response to the report ‘Master Builders Australia CEO Denita Wawn said HomeBuilder was the right policy for the time and should not become the scapegoat for systemic housing challenges.’ At the time of writing no other industry association has publicly commented on the report.

Infrastructure Spending

As well as HomeBuilder, Australian governments significantly increased spending on infrastructure during COVID. The Inquiry report found by May 2021 the Commonwealth Government had committed $14 billion to infrastructure projects, and the 2021–22 Budget included an additional $15.2 billion over 10 years for road, rail and community infrastructure. Also in 2021, the New South Wales Government committed to $100 billion in infrastructure work, and the Queensland Government announced projects worth $52 billion. In both cases the projects were expected to be completed over four years.

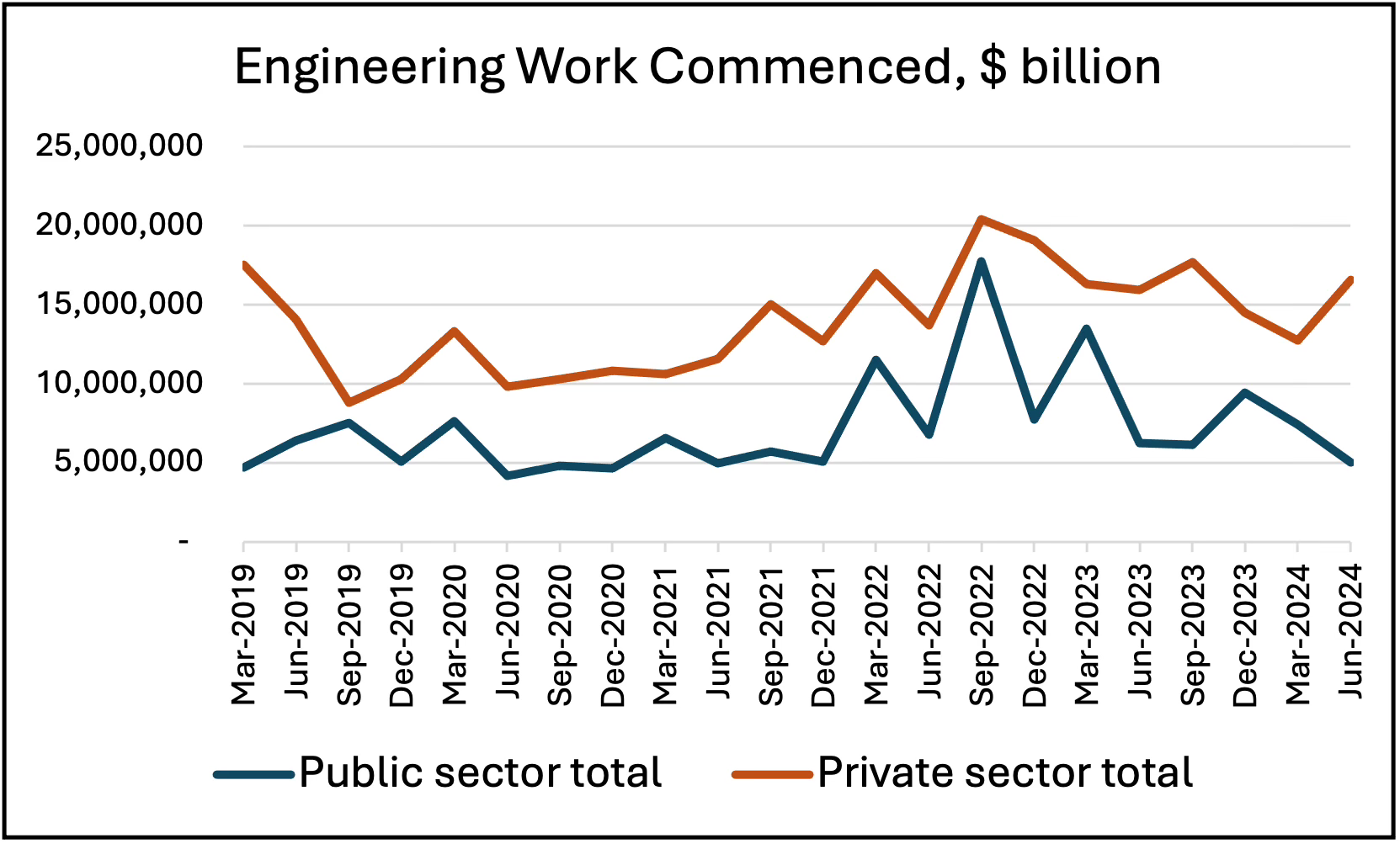

Figure 1. Engineering construction

Source: ABS 8762. Work commenced by the private sector.

As Figure 1 shows, the public infrastructure projects announced in 2021 were commencing in 2022, and in the five quarters from March 2022 to March 2023 over $57 billion of public engineering work commenced. This was an unprecedented amount, for comparison, in the 2020-21 financial year public engineering work commenced was $21 billion. In 2021 private engineering commencements also began increasing, and both public and private commencements then peaked at the same time in December 2022.

HomeBuilder National Partnership Agreement Review: Stakeholder Consultation

The 2022 review of the National Partnership Agreement (NPA) by KPMG found state and territory governments were not consulted on the design or implementation of the HomeBuilder program. The first they knew about the program was when it was publicly announced. This is somewhat ironic, given first the objective of the NPA was to create ‘a framework for the parties to work cooperatively, to provide financial assistance to eligible owner-occupiers to increase residential building and maintain jobs. No administrative funding was provided by the Commonwealth Government for establishing, running and reporting on HomeBuilder, despite the size of the program.

The states and territories were responsible for administering the program, checking eligibility, and compliance and auditing. The review found ‘This created significant implementation challenges for these jurisdictions.’ There were also significant costs associated with assessing eligibility and the principal place of residence of applicants. The report also found insufficient clarity and guidance on the income caps, in the definition of substantial renovation, on citizenship requirements, and for cases where replacement contracts were required. Treasury ‘erroneously assumed’ existing First Home Owner Grant portals could be used.

The review commented on the inflationary effect: ‘It could be said that the HomeBuilder did partially contribute to the constraints in supply of labour, materials and land that resulted from this industry overheating. However, it is critical to note that this would have been just one factor. Broader supply chain issues because of the COVID-19 pandemic were another, and much more impactful, factor.’ (p. 15).

Issues raised in the consultations with the states and territories were:

Did the eligibility criteria favour middle to high income earners?

Was offering the same amount for new build and renovations a fair approach?

Did the NPA consider state and territory ‘operating environments and industry contexts’ such as internal migration and their supply and demand balance?

Did HomeBuilder only benefit a small number of builders?

What Were the Outcomes of the Program?

The purpose of HomeBuilder was to increase residential building and maintain jobs by providing financial assistance to eligible owner-occupiers. Both of those objectives were achieved. The total number of people employed in construction in August 2020 was 1,145,814, a year later in August 2021 it had fallen to 1,114,644, but by August 2022 it was 1,251,601. Construction employment continued increasing through 2023 and 2024, reaching a record high of 1,358,239 in May 2024.

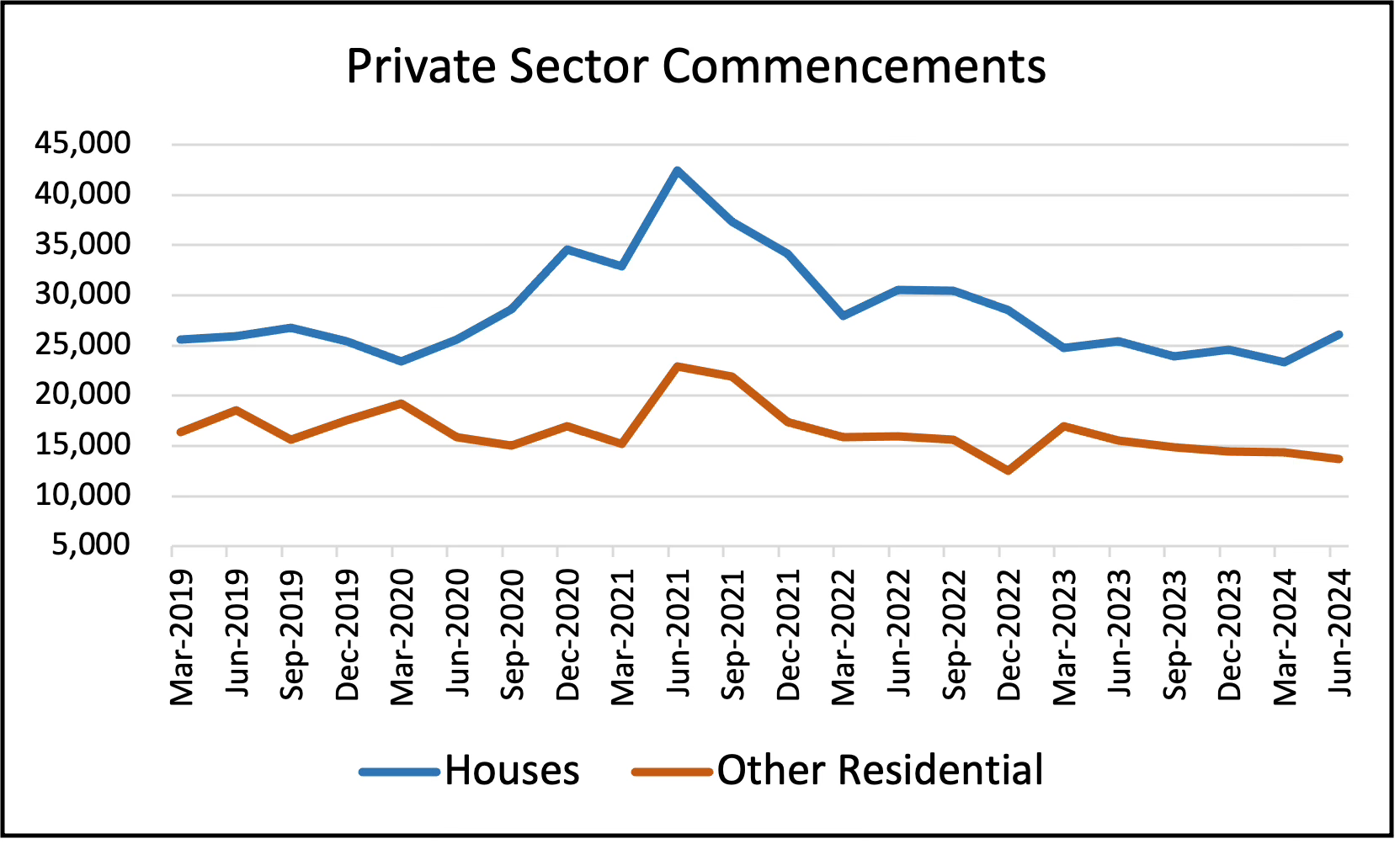

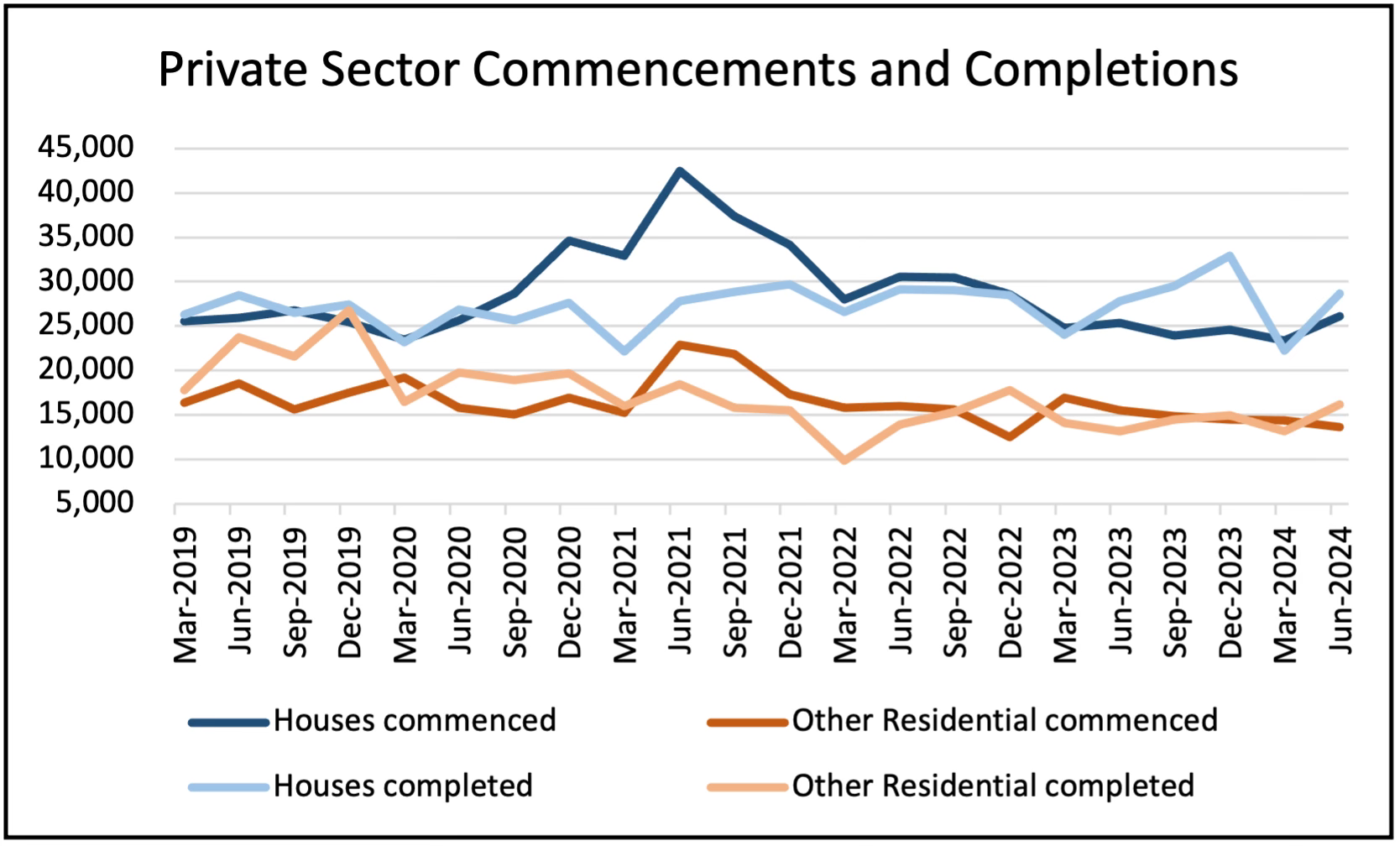

As Figure 2 shows, residential commencements increased rapidly after the program started in mid-2020. The 42,475 houses commenced in the June quarter 2021 was an all-time record, well above the quarterly commencements of around 30,000 during the housing boom between 2015 and 2018. The increase for apartments was not as dramatic, although still substantial, rising from 15,070 in the September quarter 2020 to 22,913 in the June quarter 2021.

Figure 2. Number of dwellings commenced

Source: ABS 8752

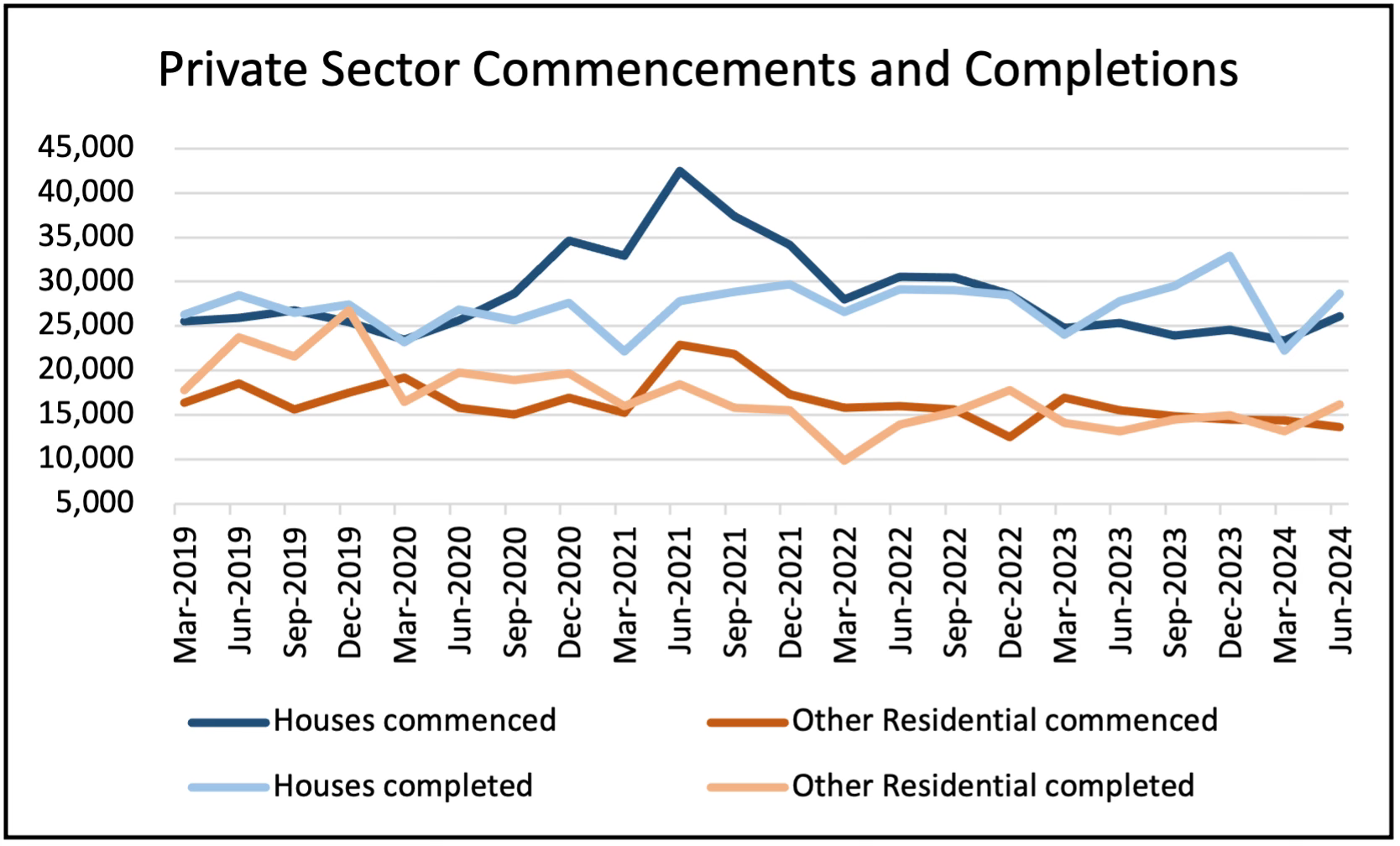

The combination of HomeBuilder induced demand with COVID supply chain disruptions had three effects on residential construction. First was the increase in completion times for houses. As Figure 3 shows, the industry usually delivers between 25,000 and 30,000 houses a quarter, less in the March quarter because of the January holiday, with most houses completed within 12 months. It took three years, until the December quarter 2023, to complete the extra 100,000 houses commenced in 2020 and 2021 during HomeBuilder [1]. There was less effect on apartment completions because the number of commencements was well below past record levels, so the volume of work was within industry capacity not above it.

Figure 3. Number of dwellings commenced and completed

Source: ABS 8752

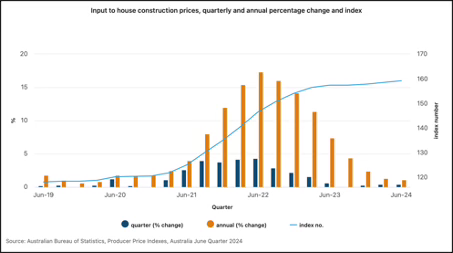

Second was the increase in the cost of inputs. Some of the materials and component price increases were due to global factors, but there were also significant increases in domestic prices and labour costs. As Figure 4 shows, the ABS input price index increased from 120 in December 2020 to 154 in December 2022.

Figure 4. Housing costs

Source: ABS 6427

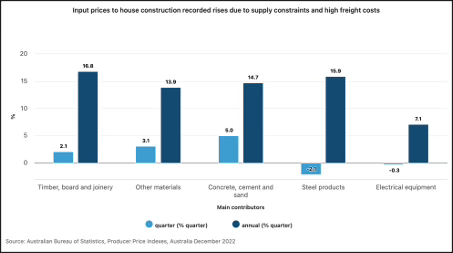

In the 12 months after the surge in commencements due to HomeBuilder, between the December quarter 2021 and December 2022, the price of basic inputs such as timber, plywood, glass, cement and steel all increased by around 15%. Some of the increase was due to higher energy and freight costs, and the other materials category was affected by plaster products because of a global price increase for gypsum. However, the main driver of these price increases was the high level of demand created by HomeBuilder and also, for concrete and steel, infrastructure projects.

Figure 5. Construction input price changes to December quarter 2022

Source: ABS 6427

The increase in house building costs differed across the states. In the Reserve Bank’s November 2024 Statement on Monetary Policy the RBA commented: ‘Labour costs continue to contribute to ongoing cost growth, partly driven by the large pipeline of construction work and ongoing labour shortages for certain trades. Outcomes have varied across capital cities. Year-ended new dwelling cost inflation has returned to around its pre-pandemic average in Sydney, Brisbane and Hobart. By contrast, new dwelling cost inflation in Perth has increased further in year-ended terms, consistent with high demand for new homes and increases in labour costs’. The accompanying graph highlights how rapid and extreme the pandemic cost increases were.

Figure 6. Capital city cost inflation

Source: Reserve Bank of Australia, Statement on Monetary Policy, November 2024.

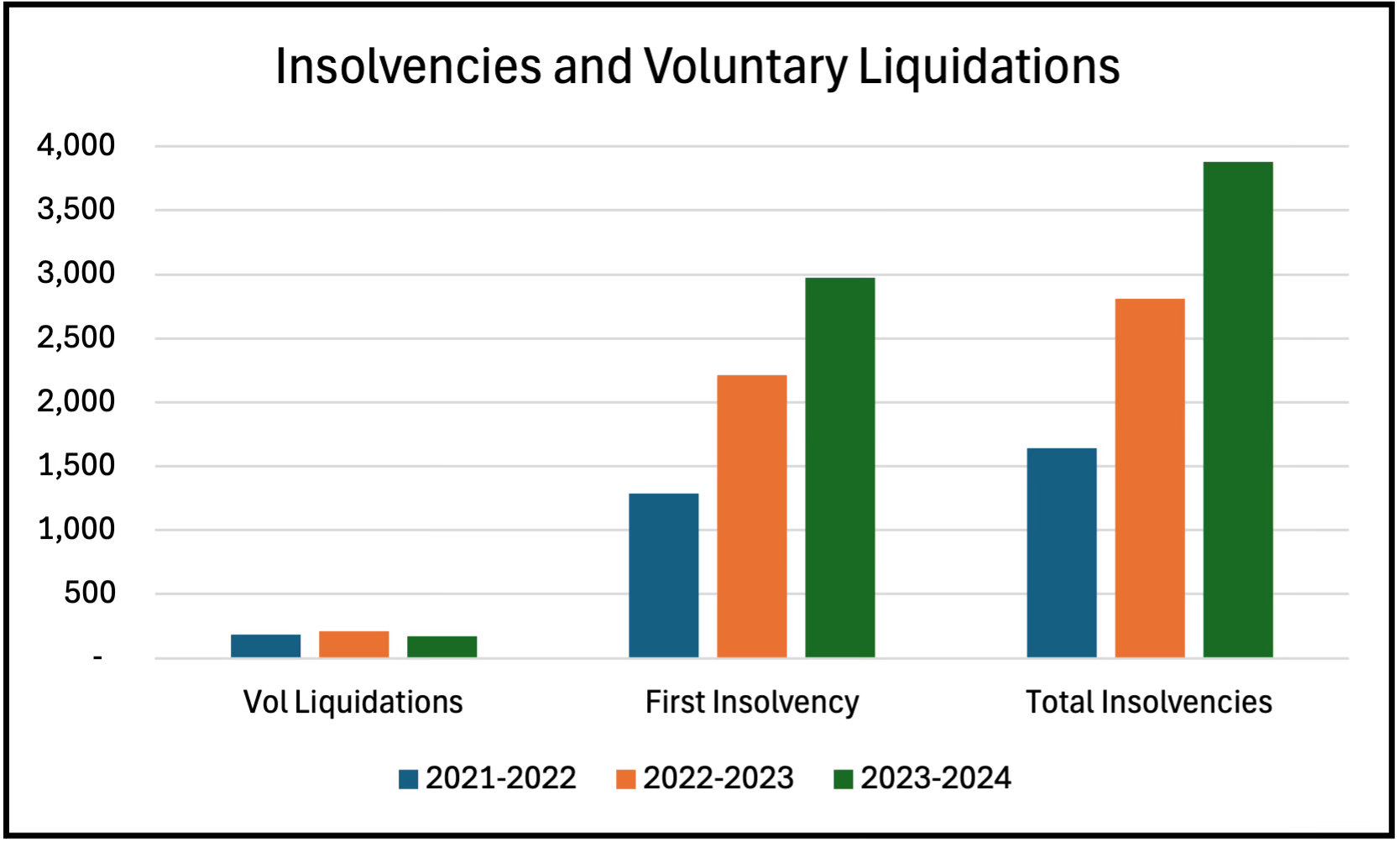

Third was the increase in insolvencies between 2022 and 2024, as many builders on fixed price contracts entered into during HomeBuilder were unable to continue after cost inflation led to losses on those projects. Because of measures put in place to support industry during the COVID pandemic there were fewer insolvencies than usual in 2021-22, with a total of 1,639 construction businesses going into administration. The numbers for 2023 and 2024 show a substantial increase in total insolvencies from 2,812 to 3,882.

Figure 7. Construction insolvencies

Source: Australian Securities and Investment Commission

Conclusion

A counter-cyclical increase in government construction expenditure is a common use of fiscal policy. However, the COVID Inquiry report concluded: ‘There are clear indications that the infrastructure measures taken – in particular, HomeBuilder – overheated the industry and contributed to inflation in the post-pandemic era.’

The purpose of HomeBuilder was to increase residential building and maintain employment, and it succeeded in both of those. There was a small decrease in total construction employment in 2021 of around 30,000, followed by a steady increase to a record 1,358,239 people in 2024. The program quickly increased housing commencements to record levels, but completion times increased and it took three years to complete the extra 100,000 houses commenced in 2020 and 2021.

The size of the program was uncapped and Treasury significantly underestimated the number of applications [2]. Their forecast for the cost of the program was $680 million, and the extension $241 million but, instead of $921 million, by June 2024 $2.6 billion had been paid. Although HomeBuilder was a minor program compared to the tens of billions spent on transfers through the Australian Tax office, it was targeted at a specific industry and administered by the states and territories.

Over time the effects of the sudden increase in commencements financed by HomeBuilder became less positive. The COVID Inquiry report focused on the inflationary effect of the rapid increase in demand on the cost of housing, which accounted for up to 50% of CPI increases in 2021-22. The report concluded the demand side stimulus was not appropriate and ignored the supply side effects. The increase in residential commencements was not only due to HomeBuilder, which combined with first home owner grants, stamp duty exemptions, and other incentives given by state governments, all of which added to the excessive level of demand.

Likewise, the increase in materials and component prices was not only due to HomeBuilder. Both the Commonwealth and the states also increased expenditure on infrastructure during COVID, which added to the inflationary effects. In the five quarters from March 2022 to March 2023 over $57 billion of public engineering work commenced, a record amount, and both public and private engineering construction commencements peaked at the same time in December 2022.

There was a notable failure in policy making in 2020, governments and their advisors should have decided to target either residential building or engineering construction for stimulus. To simultaneously do both showed a poor understanding of construction industry characteristics and capacity, and ignored the obvious domestic and international supply side constraints during the pandemic. Also, governments would have been aware of rising private sector engineering expenditure when increasing their own spending. There is no evidence of industry being consulted or asked for advice at any point while these decisions were being made.

The consequences of these poor policy decisions by state and federal governments have now become apparent. Over 8,000 construction businesses have become insolvent since 2021, many because of losses on fixed price contracts entered into under HomeBuilder, affecting thousands more customers, subcontractors and suppliers. The cost of inputs to housing construction have increased by around 30% since 2020, increasing house prices and making new houses unaffordable for many first home buyers. Further, the build cost of new apartments is now above the price of existing stock, so the apartment market is broken. Infrastructure projects have had cost increases and delivery delayed.

There is a long tradition of increasing government expenditure on construction to counter economic downturns, however HomeBuilder was not good policy. Rather, when combined with the increase in public infrastructure spending, it is an example of reactive over-reach and poorly considered policy-making. Over the last two years inflation, and therefore interest rates, would have been substantially lower without HomeBuilder, as would house prices. That may be hindsight, and with COVID the circumstances were extreme. Nevertheless, the program did not take into account the characteristics and capacity of the construction industry, and at no point attempted to address the important supply side issues the industry had to deal with. Unfortunately, the implementation and size of the program demonstrated little understanding of the industry by governments and their advisors.

[1] In the Australian Financial Review (1.11.2024) the Stockland CEO Tarun Gupta was quoted: ‘pre-COVID it took his company 16 weeks to build a home, it doubled to 32 weeks in the pandemic, and is back to 20 to 22 weeks. He dubs it a new “resistance level”. Likewise, he says civil works for a 300- or 500-lot precinct used to take 26 weeks, blew out to 42 weeks in Victoria (the worst state at the time) and is back to 32 to 34 weeks.’

[2] None of the reviews of HomeBuilder looked at the Treasury forecasts or asked why they were so far off the mark.