Investment in Physical and Intellectual Capital in 2023

Australian capex in machinery and equipment, software and R&D

The 2023 Australian System of National Accounts provided by the ABS includes data for industry investment in software, research and development (R&D), and machinery and equipment (M&E) [1]. Industry investment in physical and intellectual assets plays a vital role in economic growth through building capacity, upgrading technology, and increasing the productivity of workers.

This post compares the capital expenditure of 18 Australian industries in 2023 starting with M&E, then software followed by R&D, with industries ranked by expenditure. The ABS estimates of each industry’s net capital stock [2] are also included, with industries again ranked by expenditure. The third figure for each category compares each Industry’s share of total capital stock to the industry’s share of GDP.

Machinery and Equipment

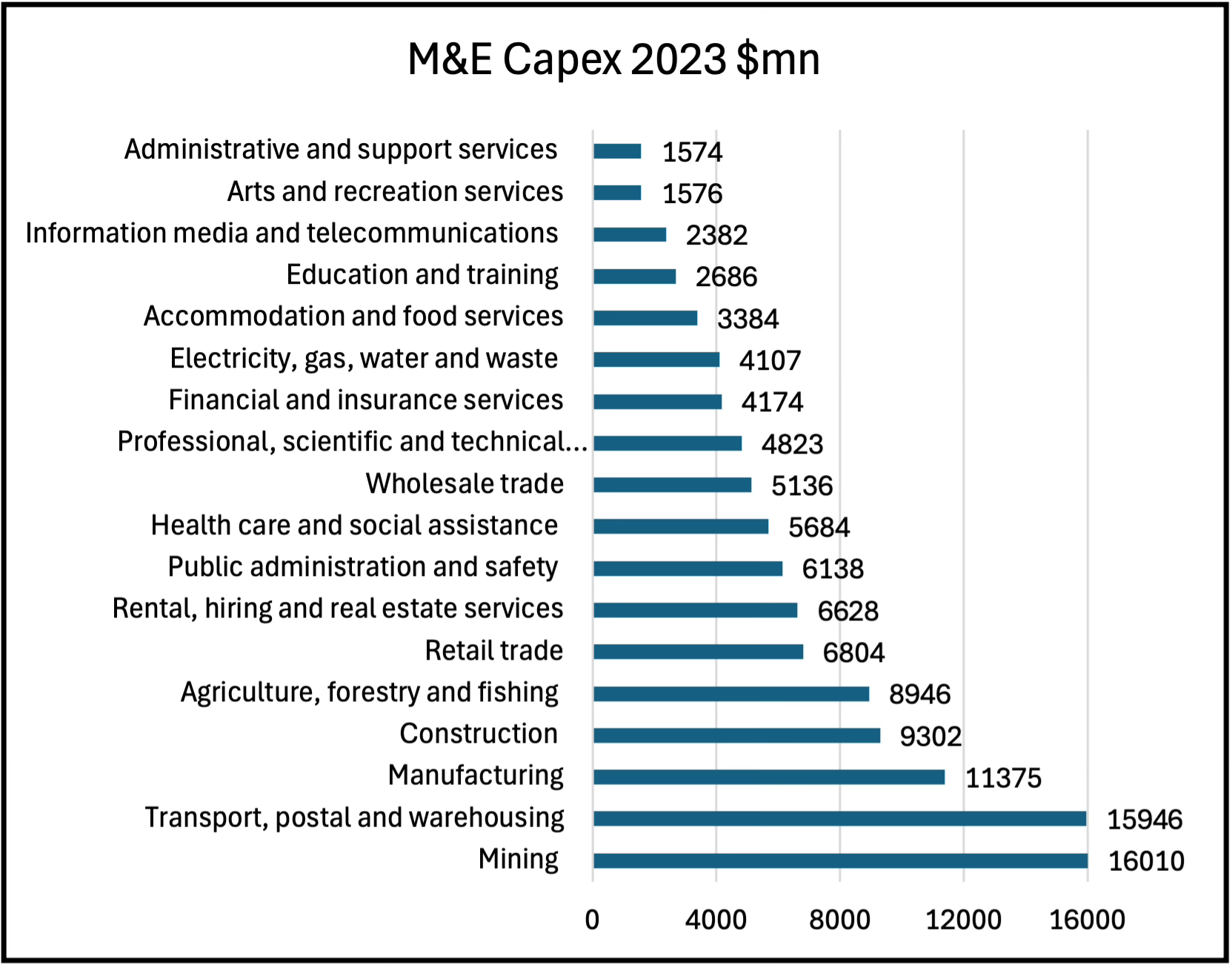

With expenditure of $120 billion in 2023, M&E is by far the most important component of investment by Australian industry. In Figure 1 Australian industries are sorted by M&E capital expenditure in 2023, from lowest to highest. The two industries of Mining and Transport spent over $15 billion, Manufacturing spent over $10 billion, and Construction and Agriculture each spent around $9 billion. Those five industries accounted for 51 percent of total M&E capex, which however is more distributed than Software and R&D capex. The next five industries include three that spent between $6 and $7 billion, and two that spent between $5 and $6 billion.

Figure 1. Industries ranked by machinery and equipment capital expenditure

Source: ABS 5204

Economic growth can come from either increased amounts of capital per worker or from technological progress and increased productivity. Since the financial crisis in 2006 the share of GDP of M&E capex has been falling, from eight to around four percent, and is now half the level it was before the financial crisis despite the decline in interest rates to 2021. With less investment the capital stock grows more slowly, leading to slower growth in output and therefore lower productivity. With a low rate of growth firms may not invest, or invest less, in expanding capacity and innovation (innovation was discussed in the previous post). The result is less economic dynamism and increasing economic inefficiency, leading to lower growth in productivity and GDP.

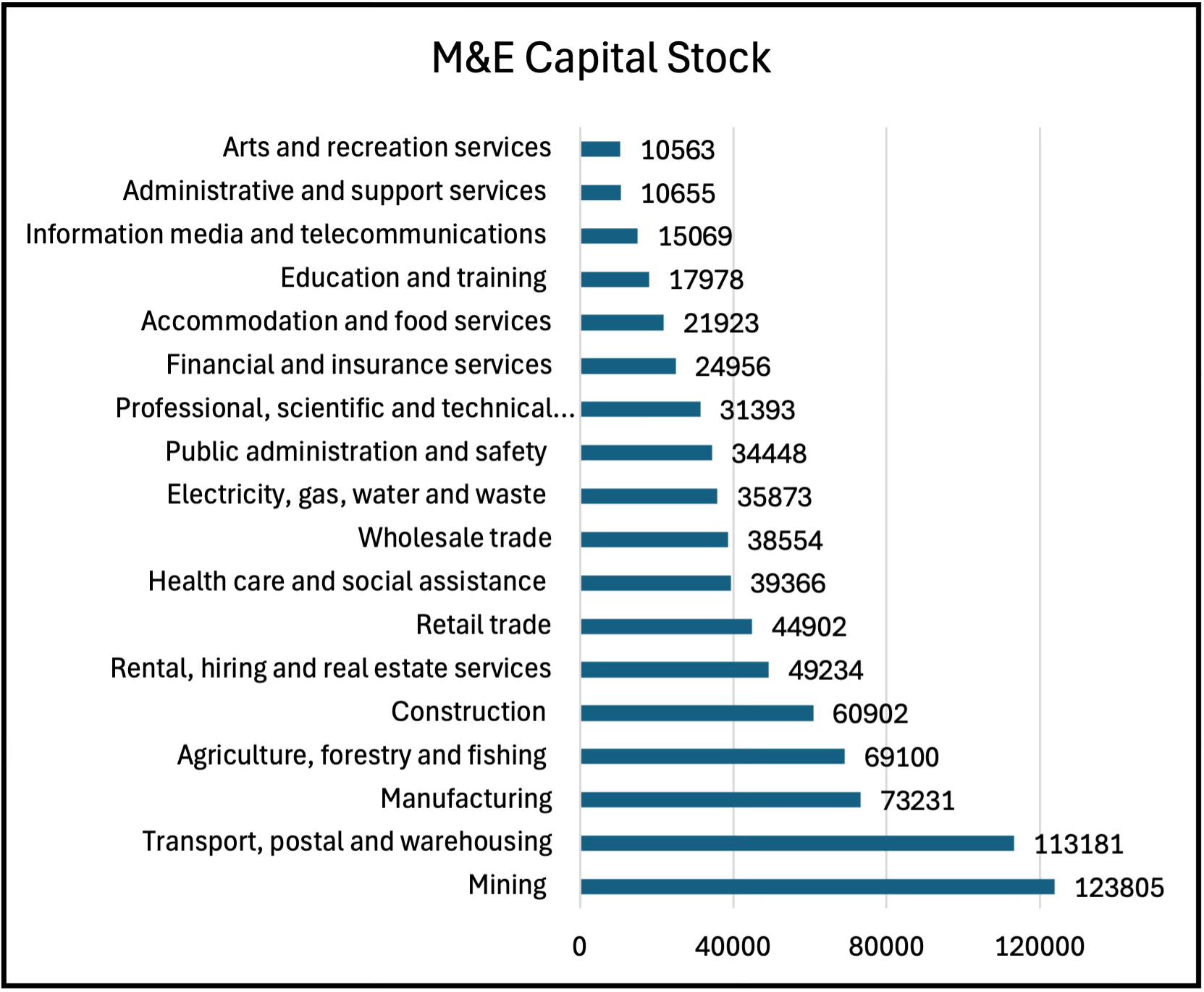

Very broadly, the net capital stock of M&E in each industry is around eight times their annual capex. Although a few industries like Electricity and Health move a couple of places, the ranking in Figure 2 generally follows that of annual expenditure. Agriculture and Construction swap places, but the top five industries are the same and they account for 45 percent of the total net capital stock. Those five asset heavy industries are by far the most capital intensive in Australia, particularly when compared with the bottom six service industries that only have between $10 and $25 billion in M&E capital stock.

Figure 2. Net capital stock of machinery and equipment by industry

Source: ABS 5204

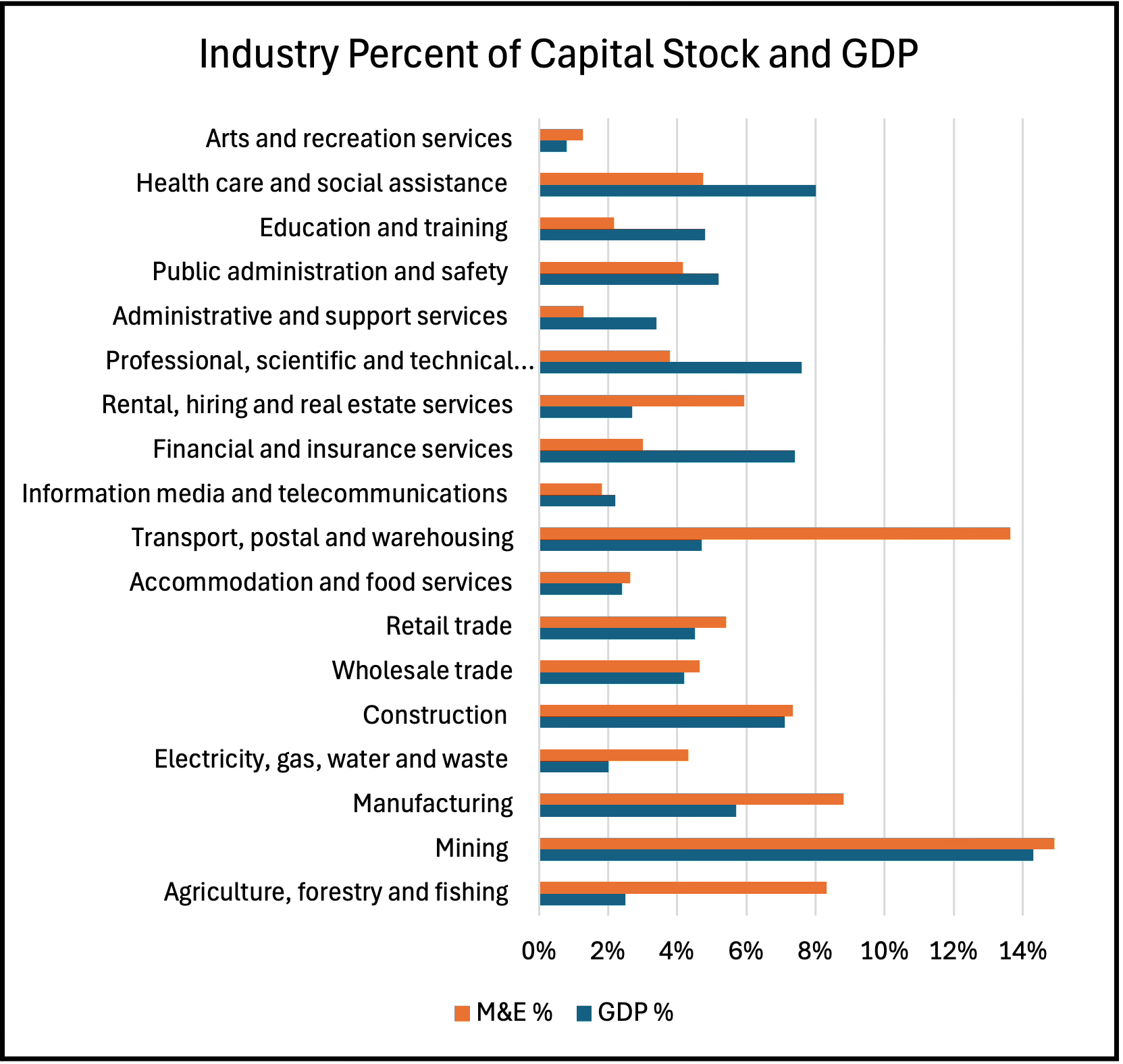

When the share of total capital stock for each industry is compared to its share pf GDP no real pattern emerges. Agriculture, Transport, postal and warehousing, and Rental, hiring and real estate services all have M&E capital stock shares that are much larger than GDP shares. Manufacturing and Electricity, gas, water and waste also have larger M&E shares. For Construction, Mining, Retail and Wholesale trades, and Accommodation and food services M&E shares are slightly higher than their GDP shares. On the other side are Health care and social assistance, Professional, scientific and technical services, Finance and insurance, and Education and training with M&E capital stock shares well below their GDP shares.

Figure 3. Industry shares of M&E capital stock and GDP compared

Source: ABS 5204. GDP in current dollars at basic prices [3].

Intellectual Property: Software

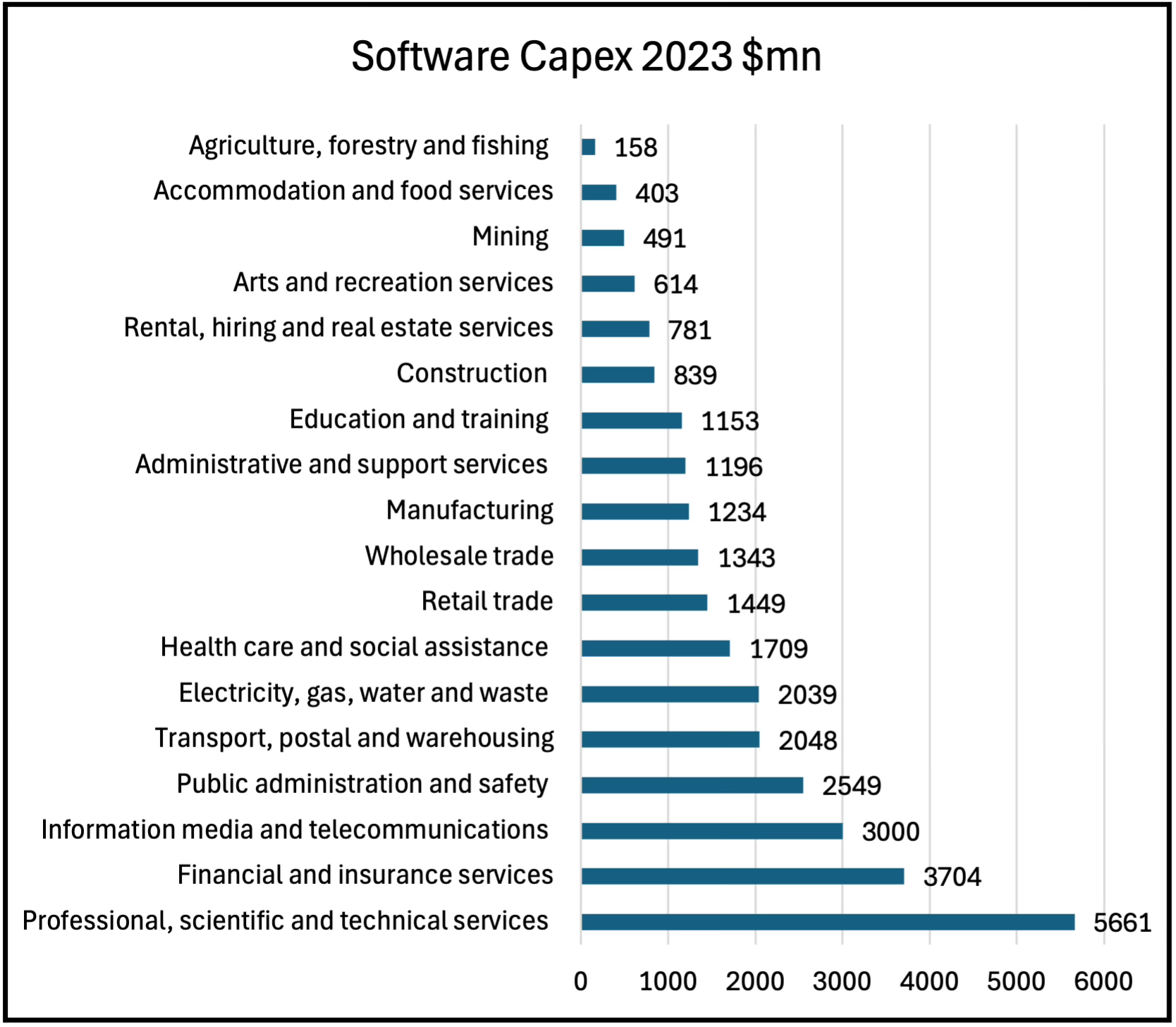

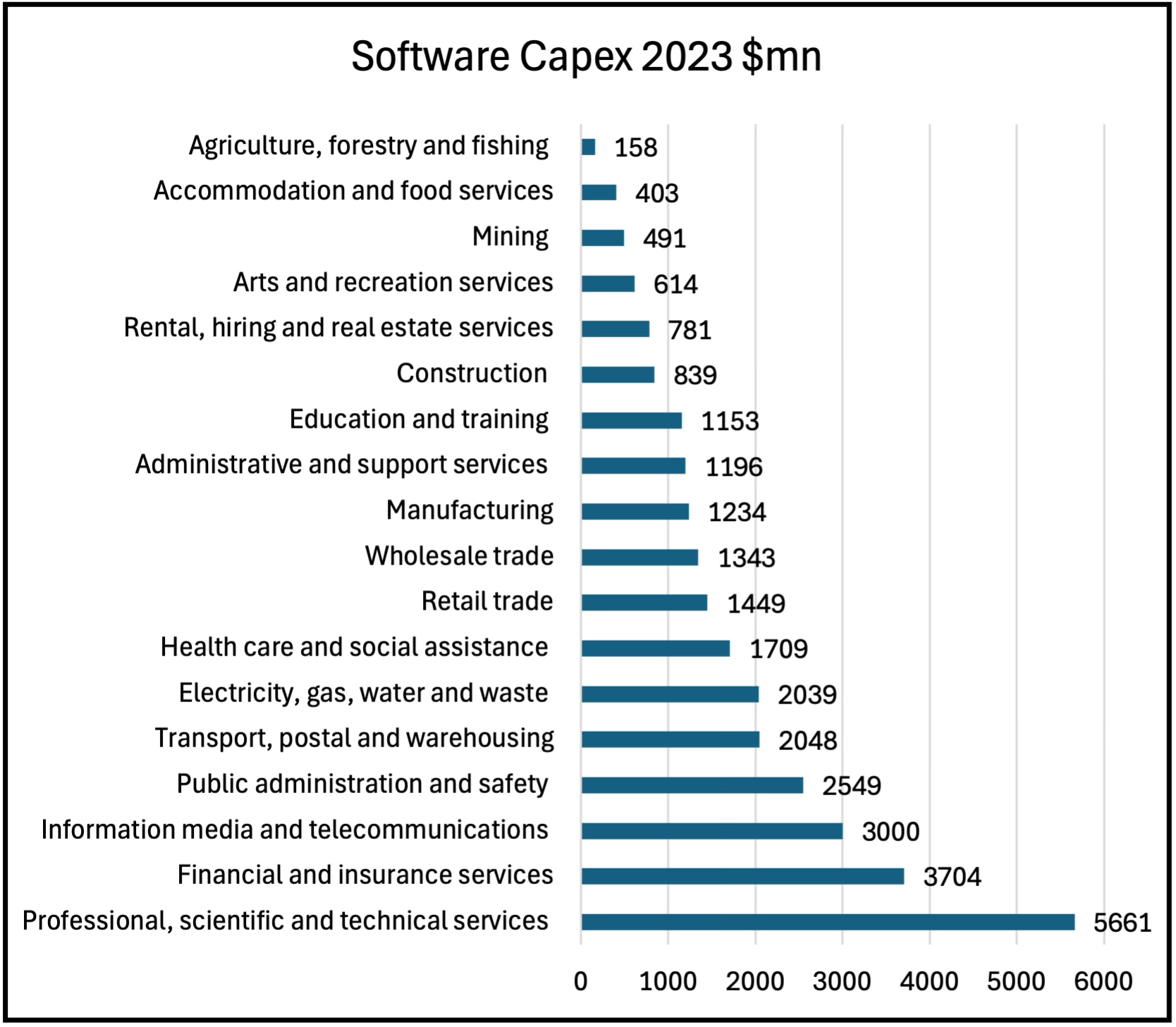

Figure 4 shows industries ranked by capital expenditure on software, which is markedly different from the M&E rankings where Mining and Transport were the largest. Professional, scientific and technical services, which includes computer systems and IT services, with $5.7 billion had the biggest expenditure. Built environment related professional services like architecture, engineering, quantity surveyors and project management are also in this industry. [4].

Finance and insurance with $3.7 billion and Information, media and telecommunications with $3 billion are the second and third largest. Three other industries spent over $2 billion, and those six industries accounted for 64 percent of the total. The top five industries accounted for 55 percent. Construction had the twelfth largest capex, and was sixth from the bottom in software capex. Total Software capex was $31 billion in 2023.

Figure 4. Industries ranked by software capital expenditure 2023

Source: ABS 5204

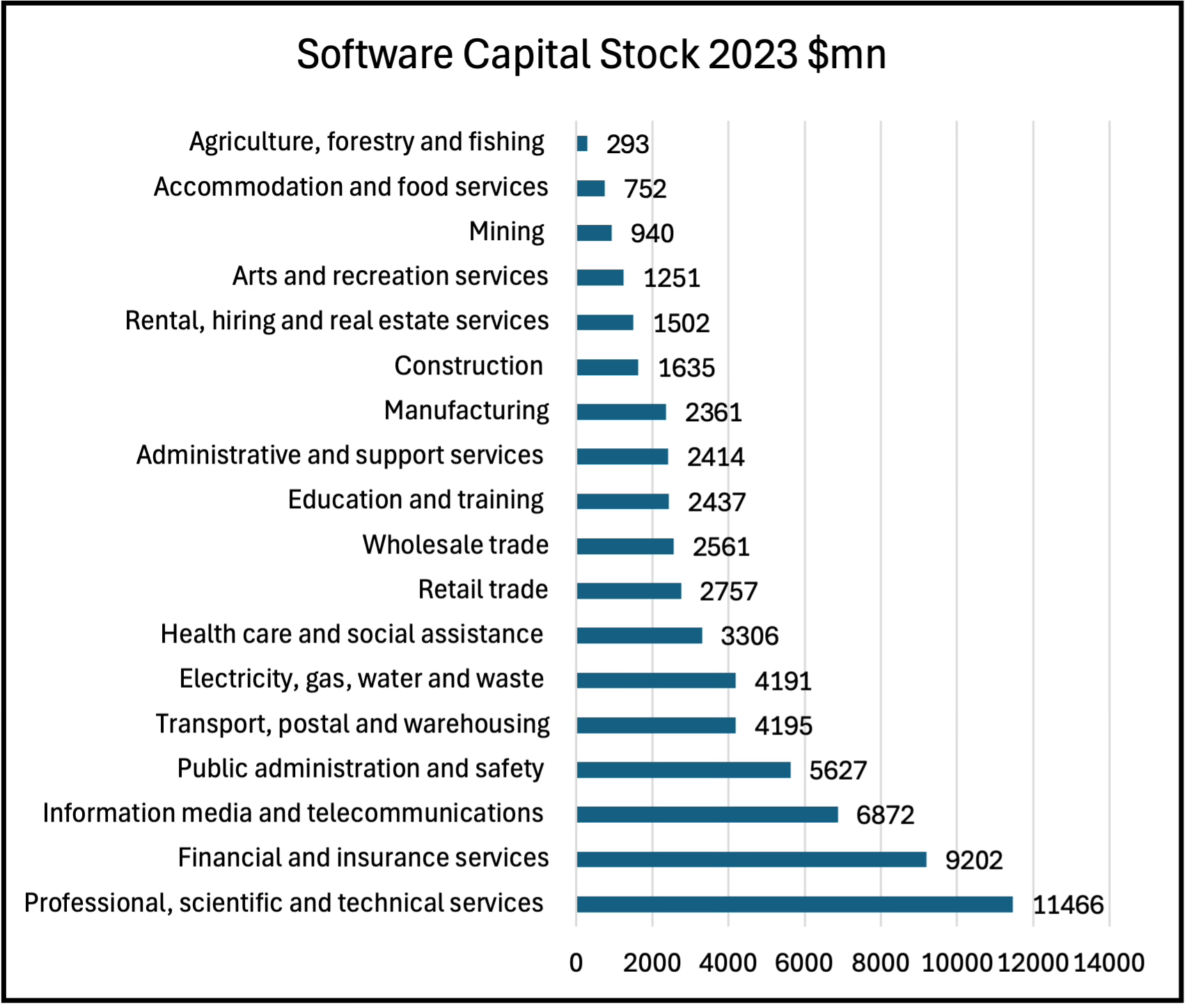

The ranking of industries by software capital stock follows that for capex, with the exception of Manufacturing, which falls a couple of places to 12. Broadly, the value of software capital stock is a bit more than twice the value of 2023 capex, indicating a rapid depreciation rate for software of around three years. The top five industries in Figure 5 accounted for 57 percent of software capital stock. Construction remains at twelfth.

Figure 5. Software net capital stock by industry 2023

Source: ABS 5204

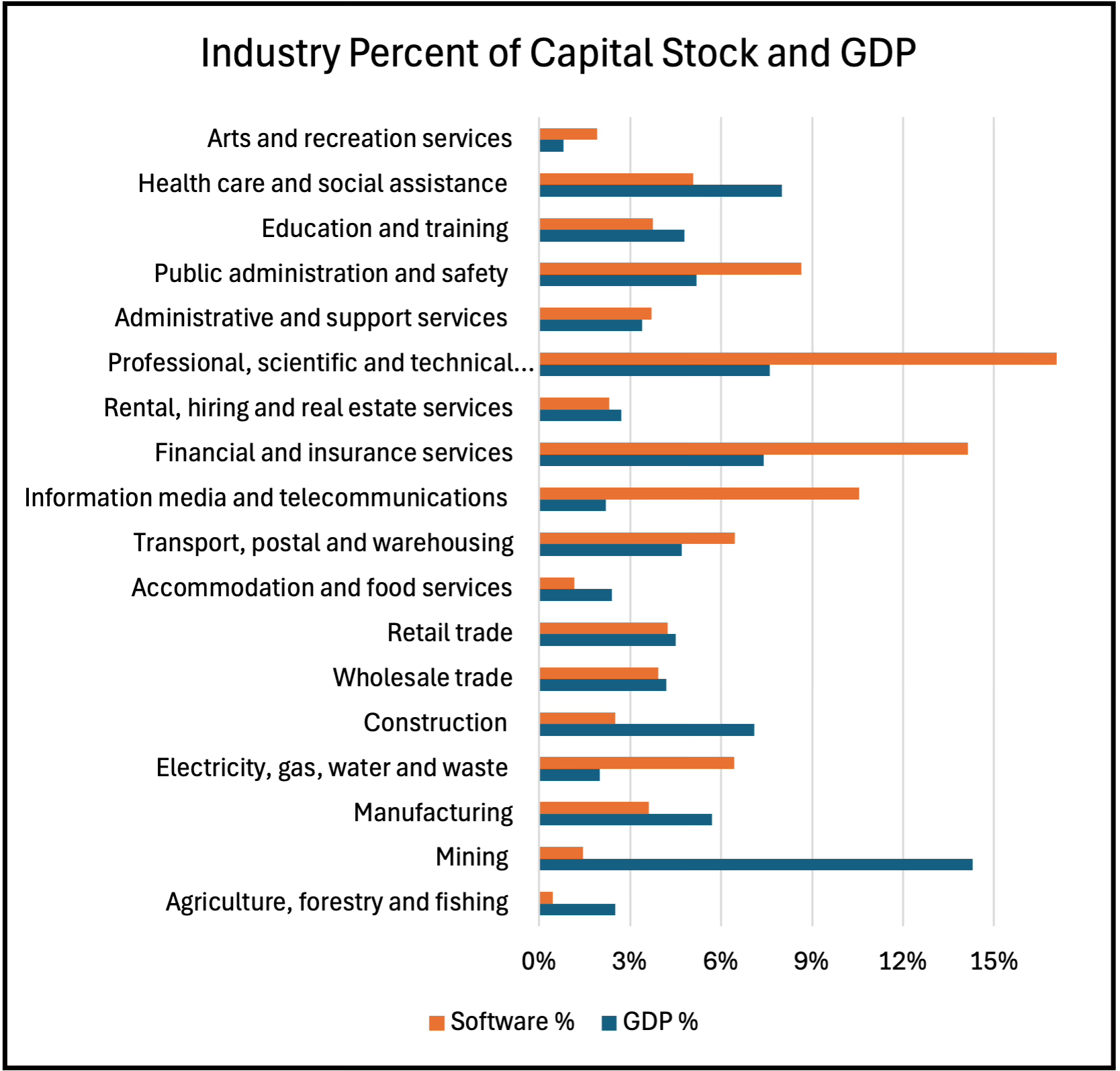

The comparison of Software capital stock and GDP shares is dramatically different to the M&E shares. Here Professional, scientific and technical services, Finance and insurance, Information media and telecommunications, Transport, postal and warehousing, and Electricity, gas, water and waste have much larger capital stock shares than GDP shares. Agriculture, Construction, Mining, Manufacturing, Education and training, Accommodation and food services, and Health care and social assistance, have smaller shares. For Retail and Wholesale trades, Rental, hiring and real estate services, and Public administration and safety the shares are similar.

Figure 6. Industry shares of software capital stock and GDP compared

Source: ABS 5204. GDP in current dollars at basic prices [3].

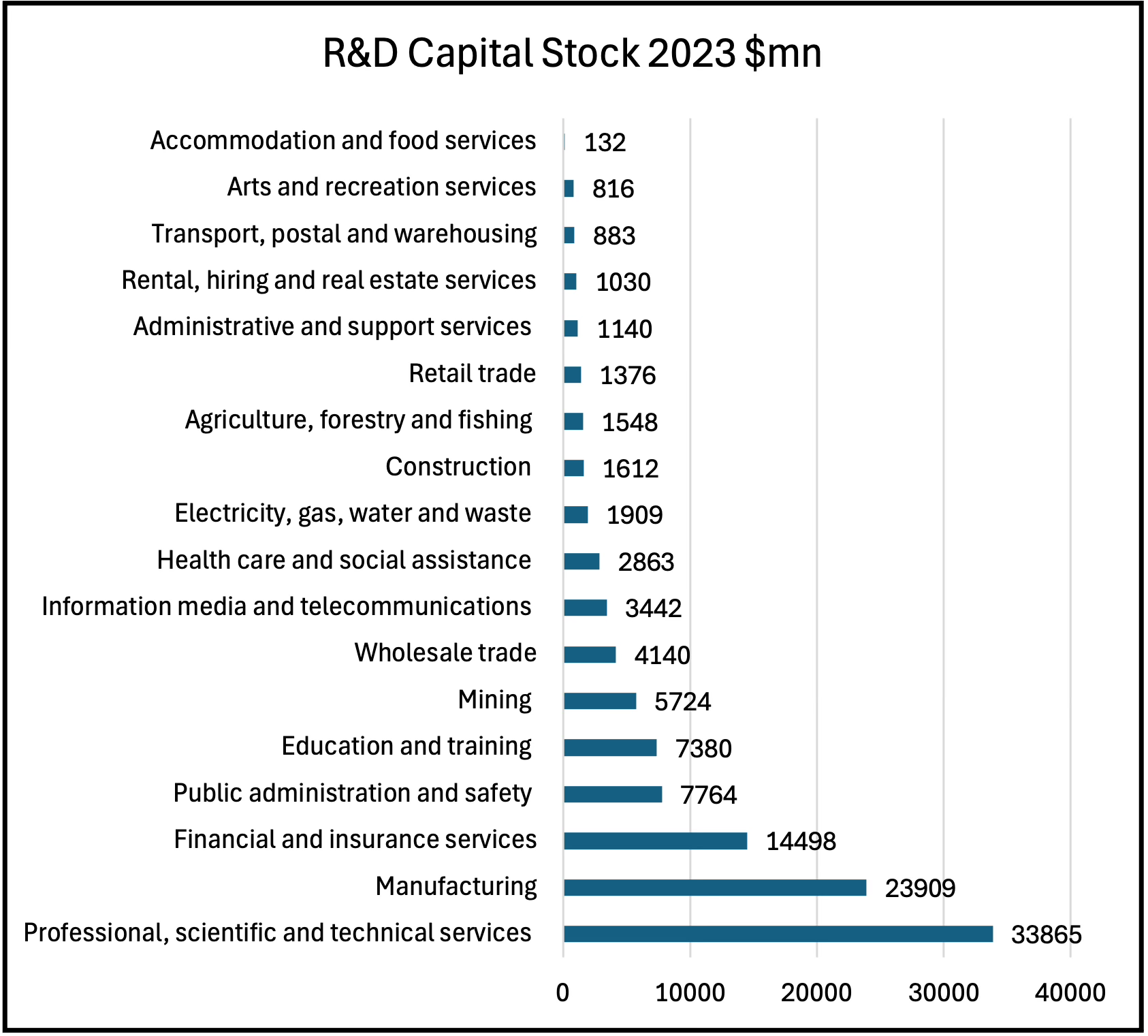

Intellectual Property: Research and Development

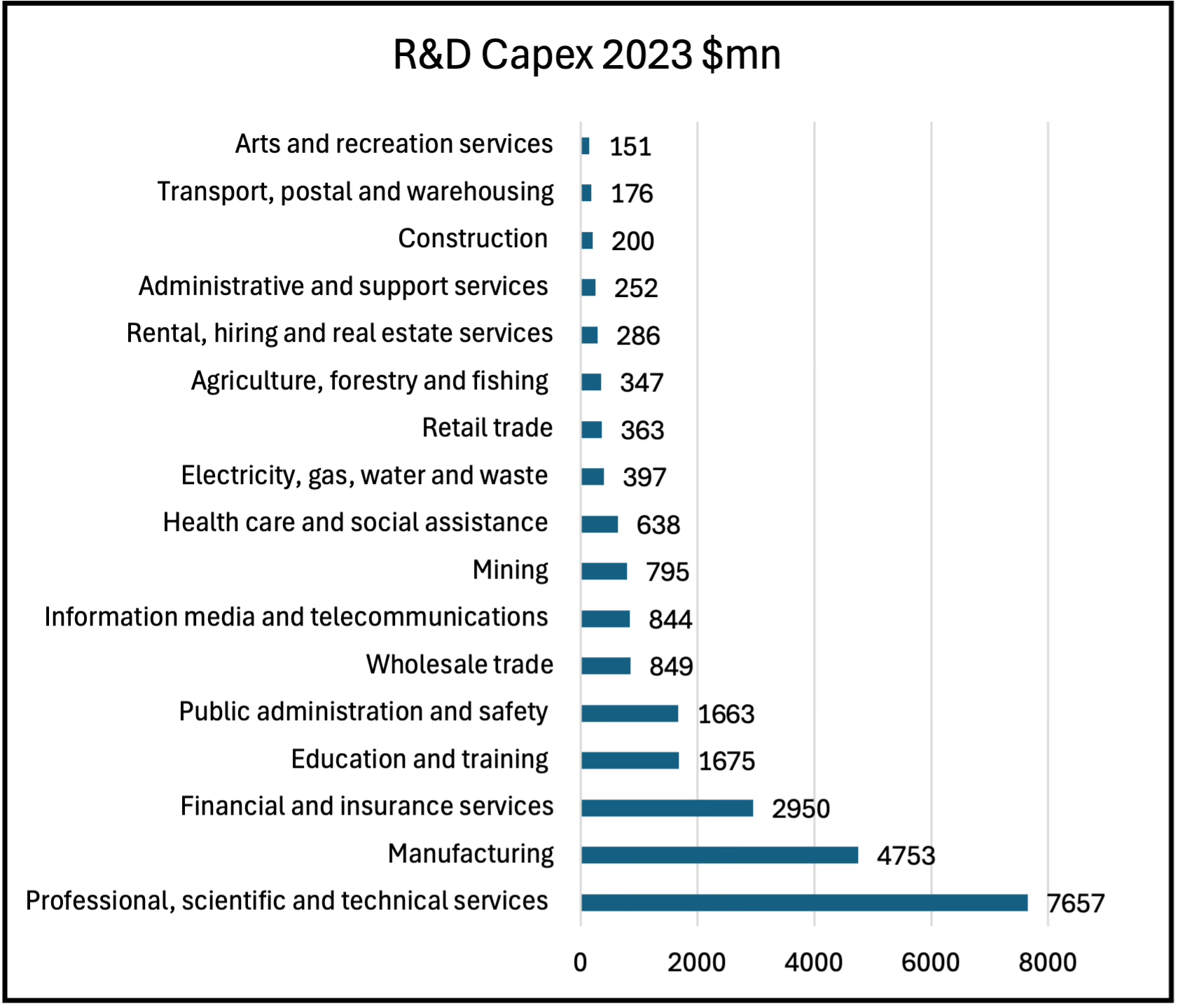

In Figure 7 industries are ranked by capital expenditure on R&D in 2023, from lowest to highest. Construction with $200 million is third from bottom and has the lowest R&D spend of any of the major goods producing industries like Agriculture, Mining and Manufacturing, which with $4.8 billion had the second largest investment in R&D. Professional, scientific and technical services, which includes the IT and computer services industries, had by far the largest R&D spend with $7.7 billion in 2023. There are five industries with capex above $1 billion, and those five accounted for 77 percent of all R&D expenditure.

Figure 7. Industries ranked by research and development capital expenditure

Source: ABS 5204

Capital expenditure on software is much more important than R&D for most Australian industries, the three exceptions where R&D was greater than software were Agriculture, Mining and Manufacturing. Some industries with low R&D capex are among the largest in software capex, such as Transport, postal and warehousing and Electricity, gas, water and waste. It is not uncommon for software capex to be many multiples of R&D, such four times more in Construction and five times more in Electricity.

The industry rankings change with the current value of R&D net capital stock, particularly for Agriculture and Mining where the value is relatively low. The leading seven industries are still leaders, Health is eight, Electricity is nineth and Construction is now at ten, ahead of Retail and Real estate services. The top five industries account for 76 percent of all R&D capital stock.

Figure 8. Net capital stock of research and development by industry

Source: ABS 5204

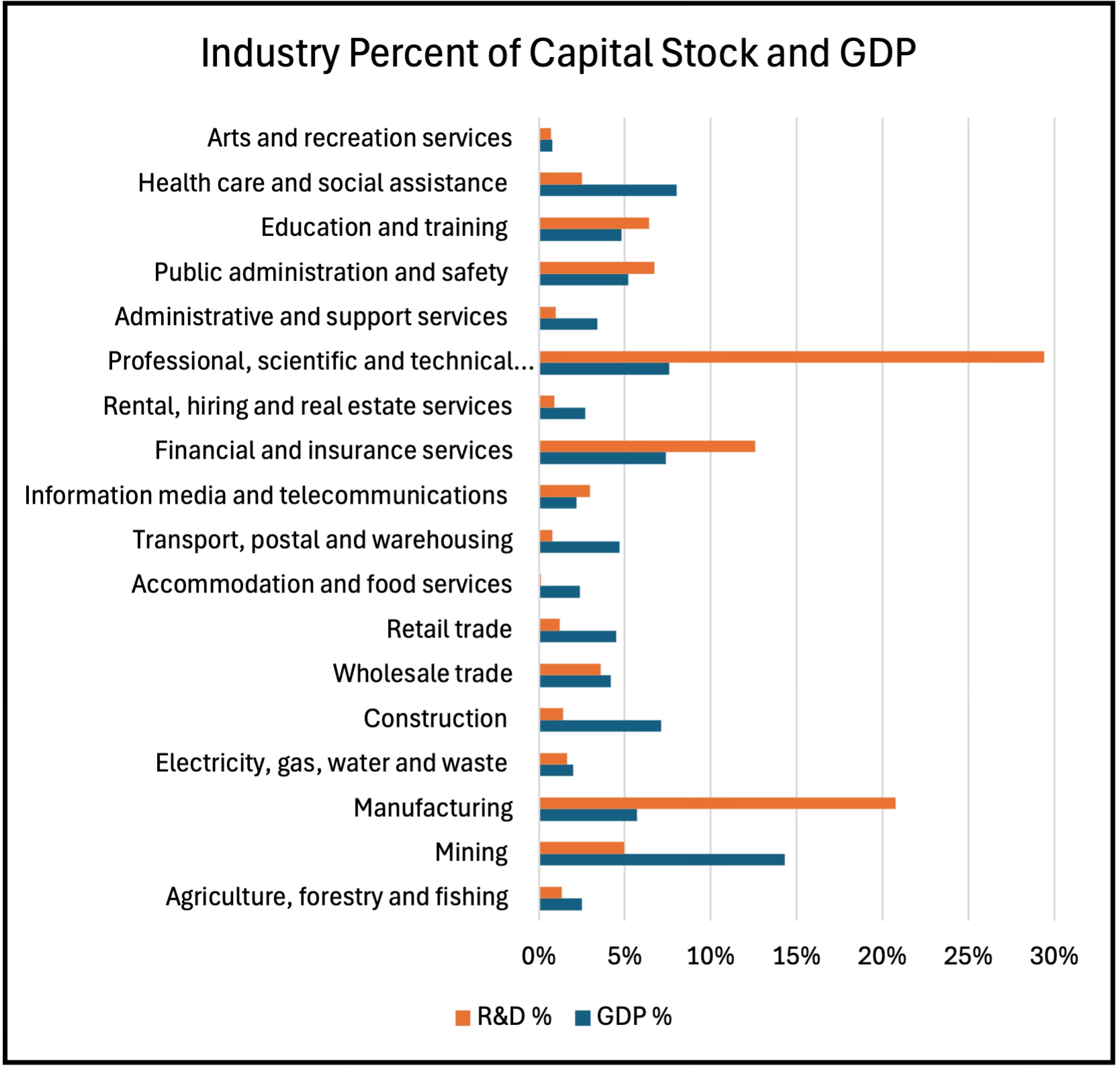

The comparison of R&D capital stock and GDP shares highlights how concentrated R&D is in Australian industry. Only three industries have significantly larger capital stock shares: Professional, scientific and technical services, Finance and insurance, and Manufacturing. Three more have slightly larger shares, Information media and telecommunications, Education and training, and Public administration and safety. For all other industries their R&D capital stock share is less than their GDP share. In industries like Agriculture, Construction, Transport, and Retail the R&D shares are much smaller than GDP shares.

Figure 9. Industry shares of R&D capital stock and GDP compared

Source: ABS 5204. GDP in current dollars at basic prices.

Conclusion

Industry investment in physical and intellectual assets plays a vital role in building capacity and upgrading technology. Between the 18 industries the ABS provides data on the level of investment varied widely in 2023, with the share of capex of the top five industries increasing from 51 percent in M&E to 55 percent in Software to 77 percent in R&D. However, different industries are in the top five.

In M&E capex in the top five industries Mining and Transport, postal and warehousing have much larger capex and capital stock than the next three industries of Manufacturing, Construction, and Agriculture. Policies to increase M&E investment could target those industries, although because M&E capex is more distributed than Software and R&D capex across the leading dozen industries a more general approach has traditionally been taken.

In Software the largest expenditure was by Professional, scientific and technical services, Finance and insurance, Information, media and telecommunications, and Public administration and safety. R&D capex is highly concentrated in a few industries. Professional, scientific and technical services, Manufacturing, and Finance and insurance had the largest expenditure. For Software and R&D, capex policies that target the top three or four industries would be most effective.

Economic growth can come from increased capital per worker or from technological progress and increased productivity. With investment the capital stock grows, and a low level of investment means slower growth in output, lower productivity, less economic dynamism and increasing economic inefficiency.

The net capital stock of M&E in each industry is around eight times their annual capex, and ranking generally follows that of annual expenditure. The ranking of industries by software capital stock also follows that for capex, with the exception of Manufacturing, and the value of software capital stock is a bit more than twice the value of 2023 capex. industries with low R&D capex are among the largest in software capex, such as Transport, postal and warehousing and Electricity, gas, water and waste. It is not uncommon for software capex to be many multiples of R&D, such four times more in Construction and five times more in Electricity. Unlike M&E and software, the R&D capex industry rankings change for net capital stock, particularly for the low capital stock industries of Agriculture and Mining.

For M&E net capital stock the top five asset heavy industries account for 45 percent of the total, and are very capital intensive compared with many service industries. The top five industries in software capital stock accounted for 57 percent. The top five industries account for 76 percent of all R&D capital stock. The comparison of R&D capital stock shares and GDP shares highlights how concentrated R&D is in Australia, with only three industries having significantly larger capital stock shares.

The industry Professional, scientific and technical services includes computer systems design and has the highest expenditure on both software and R&D, has the largest capital stock, and a much larger share of total capital stock than GDP for them. For Australia this is the leading industry for intellectual property software and R&D investment and capital stock. Because this is the industry that includes scientific research and computer systems and services this is not surprising, but the wide gap between this industry and all the others suggests it has a specific and special role in the economy, and industry policy should reflect that.

[1] The data used here is from Tables 63 and 64 of ABS 5204, which comes out in October. All figures in this post are in current dollars, but the publication includes constant dollar estimates for expenditure since 1960.

[2] Gross capital stock values each asset in use at the current price, Net capital stock is the written down value of gross capital stock. The difference between the net and gross value is accumulated depreciation.

[3] The basic price is the amount retained by the producer in respect of the good or service that is produced as output, minus any tax payable (including deductible value added taxes) plus any subsidy receivable.

[4] Professional, scientific and technical services include scientific research, architecture, engineering, computer systems design and related services, law, accountancy, advertising, market research, management and other consultancy, veterinary science and professional photography.