Industrial Strategy and Industry Policy in Australia

Part One: The policy framework and climate related funding

With the election of the Albanese Government in 2022, and its return in 2025, there has been a renewed focus on the supply side of the economy. Although the conservative Coalition Governments of the 2010s generally favoured markets over plans and industry policy, the pandemic fundamentally changed this mindset, and governments everywhere became more interventionist as they rediscovered the importance of supply chains. At the end of 2021 the Morrisson Government had three industry policies in place: the Northern Australia Infrastructure Facility (established 2016 with $5bn); and the Modern Manufacturing Initiative ($1.5bn, application guidelines opened in December 2021) and the Critical Minerals Strategy ($2bn provided in mid-2021 for new developments), both of which were overtaken by the election before any expenditures.

This post first discusses global trends in industrial policy and current thinking on policy frameworks. It then reviews two documents that have underpinned the government’s policies and two new statutory authorities. The two most significant Australian industrial policies are the Future Made in Australia included here, and the National Reconstruction Fund, to be covered in Part Two. Financing vehicles for net zero and emissions reduction are discussed next, followed by other climate and energy related policies and funding. The post concludes with the effects of the energy transition on the engineering construction industry.

A few caveats apply. First, the defence industry in Australia is another kettle of fish, or can of worms (choose your metaphor) and is not included. However, the 2026 National Defence Strategy said ‘Industry policy is security policy’ and a Defence Industry Development Strategy is due soon [1]. Second is research and development and innovation, the subject of a recent review. Generally, innovation is done by industry, often through one of the two dozen Cooperative Research Centres that are jointly funded by industry, universities and the Commonwealth. Like defence, this is a complex area and not included. Lastly, policies affecting education, training and skills are not covered. Although an important complement to industry policy, this is a different topic altogether.

Government Interventions and Industry Policy

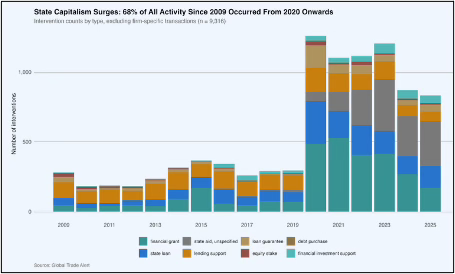

A 2026 World Bank review of national economic growth strategies in 183 countries found that all of them target at least one industry. Governments everywhere face supply-chain vulnerabilities, the digital and energy transitions, increased geopolitical rivalry and building economic resilience, so industrial policies have become more widely used, with the annual number of new industrial policies increasing from 228 in 2017 to 2,049 in 2023. Traditionally, industrial policy used tariffs and other measures to protect domestic firms from competition but, although tariffs are still important, the trend globally has been for increased use of subsidies and financial support, often channelled through government-owned agencies or intermediaries like development banks. This has been the preferred strategy of the Albanese Government. Figure 1 shows that, around the world, the number of financial interventions has greatly increased since 2020, particularly for state loans and state aid.

Figure 1. Trends in government financial interventions

Source: Global Trade Alert

The contemporary approach to industrial policy is about establishing collaboration between the public and private sectors, and developing an institutional framework within which collaboration can work. This emphasises supply of economic inputs such as energy, transport and skilled workers, with a focus on outcomes and outputs instead of processes and procedures. As the global economy reorientates away from the open borders of the last few decades towards a new era of state-based capitalism, industrial policy has become more important and is used more often, and is increasingly focused on exports and the competitiveness of firms, rather than protection from import competition.

To be competitive firms have to build capabilities, and require access to resources such as skills, research, industrial standards, capital, and infrastructure. Because these resources are public goods, they are undersupplied or not supplied by markets, thus the need for industrial policy and government intervention. There is a spectrum of policy effectiveness. In an industry with uncompetitive firms and weak institutions development cannot happen, and any intervention is likely to fail. At the other extreme, in an industry with dynamic firms and competitive strengths, policy is less important than not imposing burdens on their development. The middle ground is where firms have potential, can leverage resources created through industrial policy, and policy can compliment investment by existing or new firms.

Another important factor is state capacity and capability, which is the ability to implement policy. Because the success of industrial policy will depend on the ability of bureaucracies to interact with and exchange information with the private sector, it is capacity intensive. As well as bureaucratic capacity, bureaucratic autonomy is also important, which is the scope for agencies to independently implement and assess policies. State capacity and capability does not appear by magic and is not static, it requires repeated investment, commitment to long-term goals, criteria for success or failure, and a willingness to terminate programs and policies that either are not working or have succeeded and are no longer necessary.

Since 2022, the Australian government has rolled out a large number of industrial plans and policies, made considerable investments in specific industry capacity, established new agencies, and restructured agencies inherited from previous governments. Their actions have been broadly in line with current thinking on industrial policy, with industry consultation on development of plans, use of incentives and production credits, more funding for vocational training, finance provided through government-owned intermediaries and co-investment, and guidelines and performance measures published.

Australia’s Industrial Policy Framework

Major policy announcements are typically made in the annual Commonwealth Government Budget, in May. This has been the case for industrial policies. The 2022-23 Budget allocated $15 billion to a National Reconstruction Fund (NRF) to ‘provide finance for projects that diversify and transform Australia’s industry and economy.’ The 2024-25 Budget allocated $22.7bn to a major new industrial policy, the Future Made in Australia (FMA). There were two foundational documents that accompanied these budget announcements that have provided the supporting rationale for many, but not all, funding decisions: the 2023 Critical Technologies Statement and the 2025 National Interest Framework.

The 2023 Department of Industry Science and Resource (DISR) Critical Technologies Statement identified seven technologies:

advanced manufacturing and materials technologies;

artificial intelligence technologies;

advanced information and communication technologies;

quantum technologies;

autonomous systems, robotics, positioning, timing and sensing;

biotechnologies; and

clean energy generation and storage technologies.

The 2025 National Interest Framework is intended to guide public investment, and is structured around two streams:

the Net Zero Transformation Stream, for industries with an enduring comparative advantage where public investment is needed. Renewable hydrogen, green metals, and low carbon liquid fuels are identified; and

the Economic Resilience and Security Stream, where domestic capability is necessary and the private sector does not invest without public investment. Critical minerals processing and refining and clean energy manufacturing technologies are identified.

There are also two statutory authorities. The Net Zero Economy Authority (NZEA) is in the Department of the Prime Minister and Cabinet, and was established in December 2024 with three objectives: to promote orderly and positive economic transformation; to facilitate greenhouse gas emissions reductions; and to ensure regions, communities and workers are supported to manage the impacts, and share in the benefits, of the net zero economy. Its primary function is to support communities affected by the transition to net zero and help coal and gas workers prepare for and find new jobs. In the 2024-25 Budget the Authority’s funding was $52.2mn, and in the 2025-26 Budget was $77.4mn (from the 2025-26 PMC Budget Statement).

The NZEA targets six regions: the Hunter in NSW; Central Queensland; Latrobe-Gippsland in Victoria; Collie and the Pilbara in Western Australia; and the Upper Spencer Gulf in South Australia. These place-based policies are relatively new in Australia, and a big step up from the debacle when the car industry closed in 2016-17 and the Hazelwood coal-fired power station in the Latrobe valley shut down in 2017, with little to no support provided to their employees by the Coalition Government.

The Climate Change Authority was set up in 2011 to advise the Minister for Climate Change and Energy on greenhouse gas emissions reduction targets. It prepares the Annual Climate Change Statement to Parliament, and makes recommendations on the Carbon Farming Initiative (Emissions Reduction Fund) and the National Greenhouse and Energy Reporting System. Their 2025 Climate Policy Tracker lists over 430 policies and actions by Commonwealth and State governments and agencies. In 2024-25 the Authority had a budget of $19.3mn, almost all of which was spent on staff and running costs. This Authority does not provide any funding to industry but, because more than half of all industrial policy funding is for climate and energy related projects, it has an important role in monitoring performance.

Although Australia has signed free trade agreements with most trading partners, tariffs are still being used, mainly under the anti-dumping provisions for subsidised products. These have recently been directed at Chinese steel imports, with tariffs on steel bolts lifted to 35% for some exporters. The Australian Financial Review in April reported a tariff increase on Chinese steel reinforcing bar from 19% to 24% following a recommendation from the Anti-Dumping Commission, and in February a 10% tariff was placed on Chinese steel ceiling frames.

Future Made in Australia

The 2024-25 Budget funded the FMA and its two streams of net zero transformation and economic resilience and security, supported by the National Interest Framework released at the same time. Of the $22.7bn for the FMA, $13.7bn was for production tax incentives for critical minerals and hydrogen. These payments only go to firms that are producing output:

$7.0bn over 11 years from 2023–24, plus an average of $1.5bn per year from 2034–35 to 2040–41 for a Critical Minerals Production Tax Incentive, a refundable tax offset of 10% for the costs of processing 31 critical minerals; and

$6.7bn over 10 years from 2024–25, plus $1.1bn per year from 2034–35 to 2040–41 for a Hydrogen Production Tax Incentive of $2 per kilogram of renewable hydrogen.

The FMA legislation was passed in February 2025. In the 2025-26 budget a FMA Innovation Fund was set up.

FMA Innovation Fund

The FMA Innovation Fund is run by the Australian Renewable Energy Agency (ARENA), and provides grants to support pre-commercial innovation, demonstration and deployment of renewable energy and low emission technologies. In the 2024-25 Budget $1.7bn in new funding for the FMA Innovation Fund was provided for ARENA’s priority areas of green metals ($750mn), low carbon liquid fuel production ($450mn), and renewable energy technology manufacturing ($500mn).

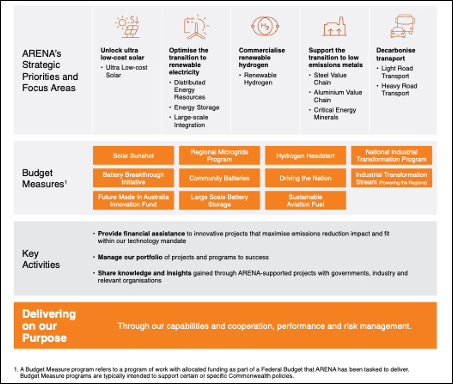

Australian Renewable Energy Agency

ARENA was established by the Gillard Government in 2012, as a renewable energy innovation agency. The 2024-25 Budget provided $1.9 bn for ARENA’s baseline funding, $1bn for the Solar Sunshot program to develop solar manufacturing, a $2bn second round of the Hydrogen Headstart program for projects producing hydrogen from renewable energy, and $500mn for the Battery Breakthrough Initiative for battery manufacturing, plus the $1.7bn FMA Innovation Fund above. This funding was continued in the 2025-26 Budget.

Figure 2. ARENA priorities and projects

Source: ARENA Investment Plan 2025.

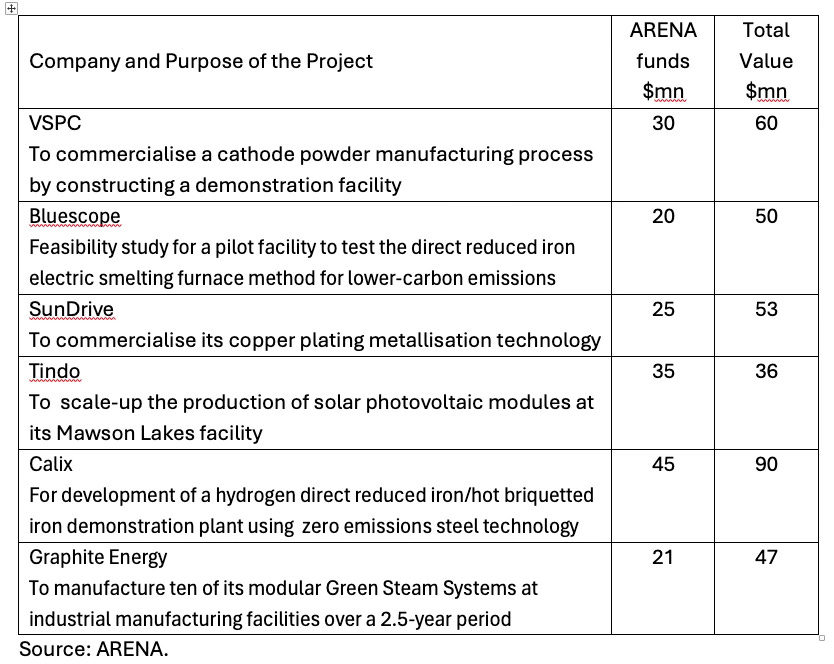

In 2025 ARENA funded 52 projects, many of which are for energy efficiency and in most cases for around half the total project value. Of the 52 projects, 5 got under $1mn, 26 between $1mn and $5mn, 8 between $6mn and $10mn, and 13 projects got over $11mn. There are two big energy projects: the Fortescue Solar Innovation Hub in the Pilbara got $45mn towards its total of $500mn (the goal is net zero by 2030 for Fortescue’s operations there); and the Battery Energy Storage System at Gnarwarre, Victoria, got $15mn of its total $351mn. As Table 1 shows, several of the largest ARENA funded projects are aligned with the manufacturing focus of FMA.

Table 1. Some manufacturing projects funded by ARENA

Source: ARENA.

Clean Energy Finance Corporation

The CEFC is Australia’s ‘green bank’ and was established by the Gillard Government in 2012, saved from abolition in 2014, and has since invested over $18bn, with $5.9bn repaid to date. Their 2024-25 Investment Update had a total transaction value of $85.3bn including co-investors. The government provided the CEFC $2.8bn in 2024 to invest in the Rewiring The Nation Fund for electricity transmission projects, and a $2bn capital injection in January 2025. The CEFC finances both large and small projects, ranging from solar farms and batteries to discounted household energy upgrades and asset finance for agriculture and industry.

Net Zero Fund

Set up in February 2026 as a sub-fund of the National Reconstruction Fund (NRF), the $5bn Net Zero Fund will use the $3bn allocated to renewables and low emissions technologies in the NRF’s $15bn allocation, and is due to be operational in mid-2026. It will be more concessional, with a target rate of return of the 5-year government bond rate minus 1% compared to the NRF’s target rate of return of the 5-year government bond rate plus 2-3%.

‘The Net Zero Fund will deliver targeted investments to support the transition to less carbon-intensive manufacturing and production processes. It will focus on supporting large-scale industrial facilities to decarbonise, improve energy efficiency and transition to net zero. The Net Zero Fund will support the Industry Sector Plan that identifies the subsectors that represent the greatest opportunity and need for decarbonisation, and those most impacted by the economy’s transition’.

The Industry Sector Plan was developed by DISR and the Department of Climate Change, Energy, the Environment and Water (DCCEEW) as part of the Net Zero Plan. There are six sector plans on decarbonisation pathways for: electricity and energy; industry; resources; transport; agriculture and land; and built environment.

Other Climate Related Industrial Plans

National Battery Strategy

The 2024 Budget launched National Battery Strategy in DISR. As well as the $523.2mn ARENA Battery Breakthrough, to promote development of battery manufacturing, there was $20.3mn for Building Future Battery Capabilities to enhance industry and research collaboration, and $5.6mn for the Australian Made Battery Precinct in Queensland.

Cleaner Fuels Program

In September 2025 a $1bn Cleaner Fuels Program was announced by DCCEEW to provide grants to Australian producers of low carbon liquid fuels, with the first application round expected in the 2026–27 financial year. The Program includes the existing $33.5mn Sustainable Aviation Fuel Funding Initiative and $250mn through the FMA Innovation Fund. When the war with Iran began in March 2026, there were three refineries making biodiesel and three making ethanol to mix with petrol, and ARENA had invested in three sustainable aviation fuel refineries in advanced planning or under construction.

Green Steel and Aluminium

The 2025-26 Budget included $2bn for green aluminium production credits and $1bn for the Green Iron Investment Fund.The Green Aluminium Production Credit is available from 2028–29, to support aluminium smelters transition to renewable electricity.

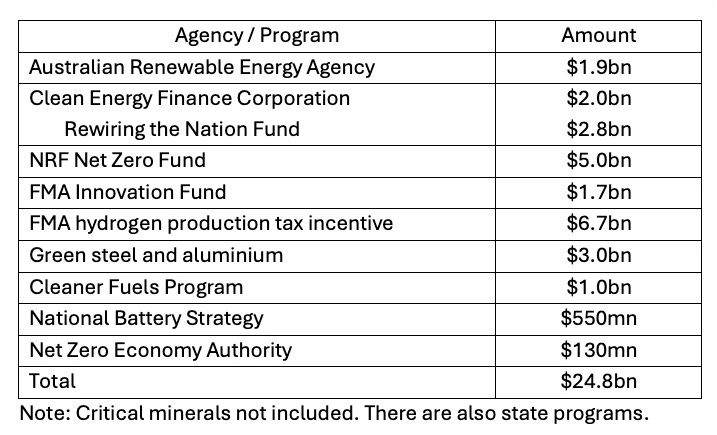

Total Climate Related Funding

Current industrial strategy and policy in Australia has a strong emphasis on funding for the energy transition. Two ongoing financing agencies are important, the Australian Renewable Energy Agency and the Clean Energy Finance Corporation. Other funding is within the NRF and FMA, and there is specific funding for aluminium, steel, fuels, and batteries. An estimate for total climate related policy funding is in Table 2. Note that outside ARENA projects, an unknown but large proportion of this $24.8bn will not have been spent, because these programs are still early stage in their implementation and many are still open for applications.

Table 2. Commonwealth energy and climate related funding since 2023

Note: Critical minerals not included. There are also state programs.

In a January media release reviewing 2025, Chris Bowen, Minister for Climate Change and Energy, said ARENA ‘supported $1.2 billion under Hydrogen Headstart plus a further 34 projects were funded to kickstart more than $420m across the innovation pipeline’ and the CEFC invested ‘more than $6.6 billion across more than 30 transactions.’

Industry in general is starting to see the benefits of the energy transition, because wholesale power prices have declined as grid batteries replace gas peaking plants. In the December quarter 2025, renewables provided just over half and in the March quarter 2026 provided nearly half of all electricity in Australia. Rooftop solar generating capacity is now greater than coal fired power, and in 2025 360,000 home batteries were installed with $3.3bn in government subsidies. Also, oil supply disruptions have less effect: after Russia invaded Ukraine power prices increased by 200% in Australia, but with the war in Iran there has so far been no effect on power prices. However, industries like agriculture, mining and transport are still heavily reliant on diesel, and these are the ‘hard to abate’ industries that have yet to decarbonise.

Effect on Demand for Construction

In the January media release Chris Bowen said 54 renewable energy projects had been approved in the year to 30 November, taking the total to 123 since 2022. ‘The Australian Energy Market Operator’s latest Connections Scorecard shows the development pipeline for the main national grid has expanded to 275 projects, representing a total of 56.6 GW in generation and storage capacity. 23.2 GW of earlier-stage projects are finalising contracts or under construction.’

The September quarterly report from the Clean Energy Council had 80 renewable electricity generation projects that have either reached financial commitment or are under construction, and 74 standalone or hybrid storage projects in the pipeline. The total number of projects was 142 and the total investment was $37.8bn, most of which is in NSW, Victoria and Queensland with over $9bn invested in each of those states.

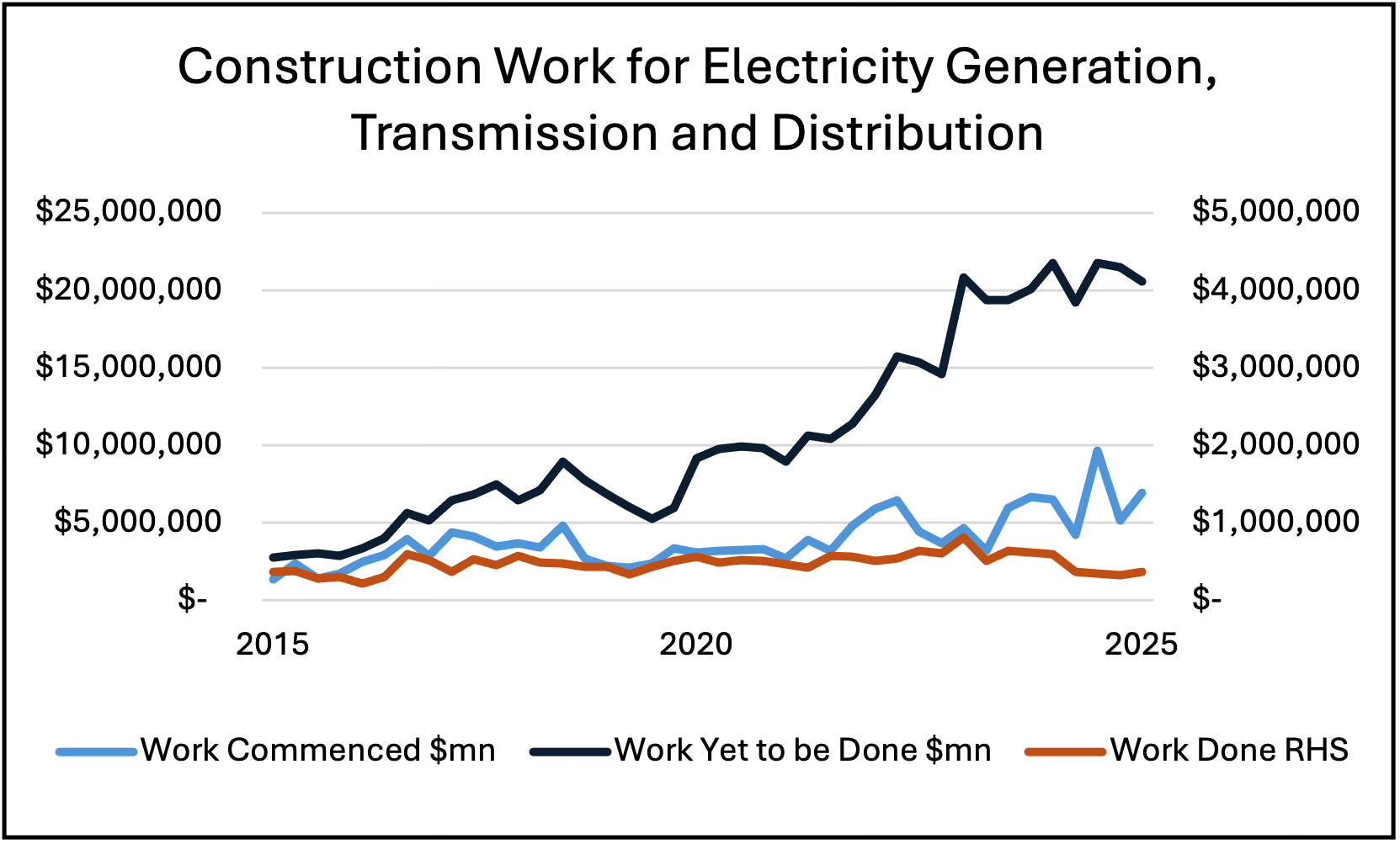

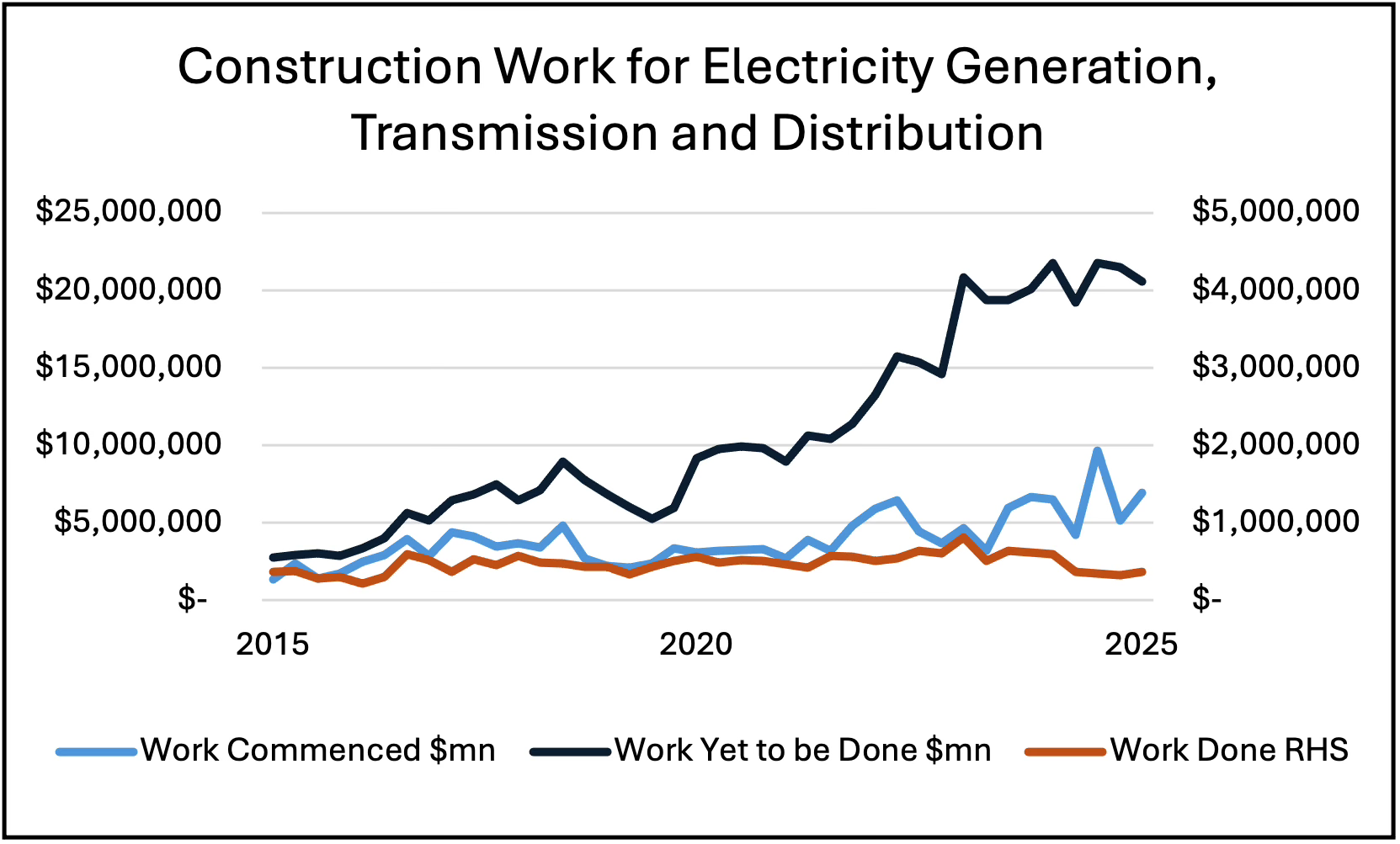

The significance of climate and energy related projects can be seen most clearly in the value of Electricity generation, transmission and distribution engineering work. Broadly, the value of work commenced and work yet to be done doubled between 2015 and 2020, and then doubled again between 2020 and 2025. The June quarter 2025 was an all-time record of $9.7bn work commenced, and there was $21.8bn of work yet to be done.

Figure 3. Engineering construction, Australia, quarterly.

Source: ABS 8762, Table 6.

From the beginning of 2023 to December 2025, $73.3bn of work commenced. Although this work includes the value of plant and machinery, the construction industry has seen a very large increase in demand. However, despite the continued increase in the value of work commenced and yet to be done, the value of work done each quarter declined in 2025, from $500-$600mn a quarter in 2024 to around $350mn a quarter in 2025.

With the high level of demand for Electricity generation, transmission and distribution work, it is worth asking why the engineering construction industry has not increased the quarterly value of work done. The values above in Figure 3 are not adjusted for inflation, so the decline in the real value and volume of work done will have been larger than those current dollar values. (The ABS does not provide chain volume measures for type of work). There is obviously a capacity constraint, and competition for resources with major transport infrastructure projects. The Clean Energy Council says 25,000 people are currently employed in clean energy and another 40,000 workers are needed by 2030. Another issue is the time it is taking to get approvals completed and work started on major energy projects.

Conclusion

Since it was elected in 2022, the Albanese government has launched a series of industrial plans and policies. These have broadly been in line with current thinking on industrial policy, with industry consultation, use of incentives and production credits, funding for vocational training, and finance provided through government-owned intermediaries and co-investment.

The energy transition is central to Australia’s industrial strategy but, because interventions are spread across a number of agencies and programs, the scale of the strategy is not obvious. Since 2023 the Commonwealth Government has committed nearly $25 billion in climate and energy related funding, and the private sector has invested perhaps $30bn in electricity generation, storage and transmission. This investment has begun to deliver, in the six months to March 2026 around half of electricity produced came from renewables.

The engineering construction industry has been a major beneficiary of the energy transition, with $73bn of work commenced on electricity generation and storage over the two years to December 2025. However, the quarterly value of work done declined in 2025, from $500-$600mn in 2024 to around $350mn a quarter in 2025. Capacity constraints and competition for resources with major transport infrastructure projects are important issues for the industry, as are complex and lengthy approvals processes for major energy projects.

*

This concludes Part One of Industrial Strategy and Industry Policy in Australia. Part Two will cover projects the NRF has funded, other industry plans, the six bailouts for steelworks and smelters, and look at some unused policy options and responses to the war with Iran. Because it will be after the 2026-27 Budget, new policies or modifications to existing ones will be included.

[1] For analysis of Australia’s defence industry the Dead Reckoning Substack posts on defence supply chain anatomy are recommended. A recent post on The Hollow Base said: ‘Industrial capacity is not a stock variable replenished by investment decisions. It is an emergent property of an ecosystem: distributed skills, supplier networks, research institutions, and the cultural practice of making things, typically accumulated across generations. Ecosystems hollowed over four decades do not reconstitute themselves on a ten-year defence planning horizon.’