Entry, Exit and Insolvencies in Australian Construction

The number of businesses is at a record high

There has been a lot of attention on the increase in insolvencies of Australian construction businesses. In 2023-2024 the number of insolvencies was 3,882, which was the highest number across all industries, and the construction share of total insolvencies was 26 percent. However, the reporting of these numbers usually does not include any context, and therefore lacks perspective. Focusing on the number of insolvencies can be misleading if industry characteristics are not also considered.

This post compares the insolvencies data from the Australian Securities and Investment Commission (ASIC) with the data available from the Australian Bureau of Statistics publication Counts of Australian Businesses. The ABS data gives the number of businesses that enter and exit each quarter, and the number of businesses operating at the end of each quarter. It is published quarterly with data that goes back to June 2020 in its current form.

The ABS data is based on Australian Business Number (ABN) registrations and sourced from Australian Tax Office records of businesses that file a business activity statement and pay Goods and Services Tax (GST). An entry is an ABN that starts paying GST or restarts after a break of more than five quarters. An exit is an ABN that is no longer actively trading because the business has cancelled their ABN, ceased remitting GST, or the ABN has changed due to a merger or acquisition. Therefore exits occur when a business has closed, has been sold, has significantly changed structure, or is no longer operating in Australia. Importantly, insolvencies are only a small proportion of the number of exits.

Construction Insolvencies

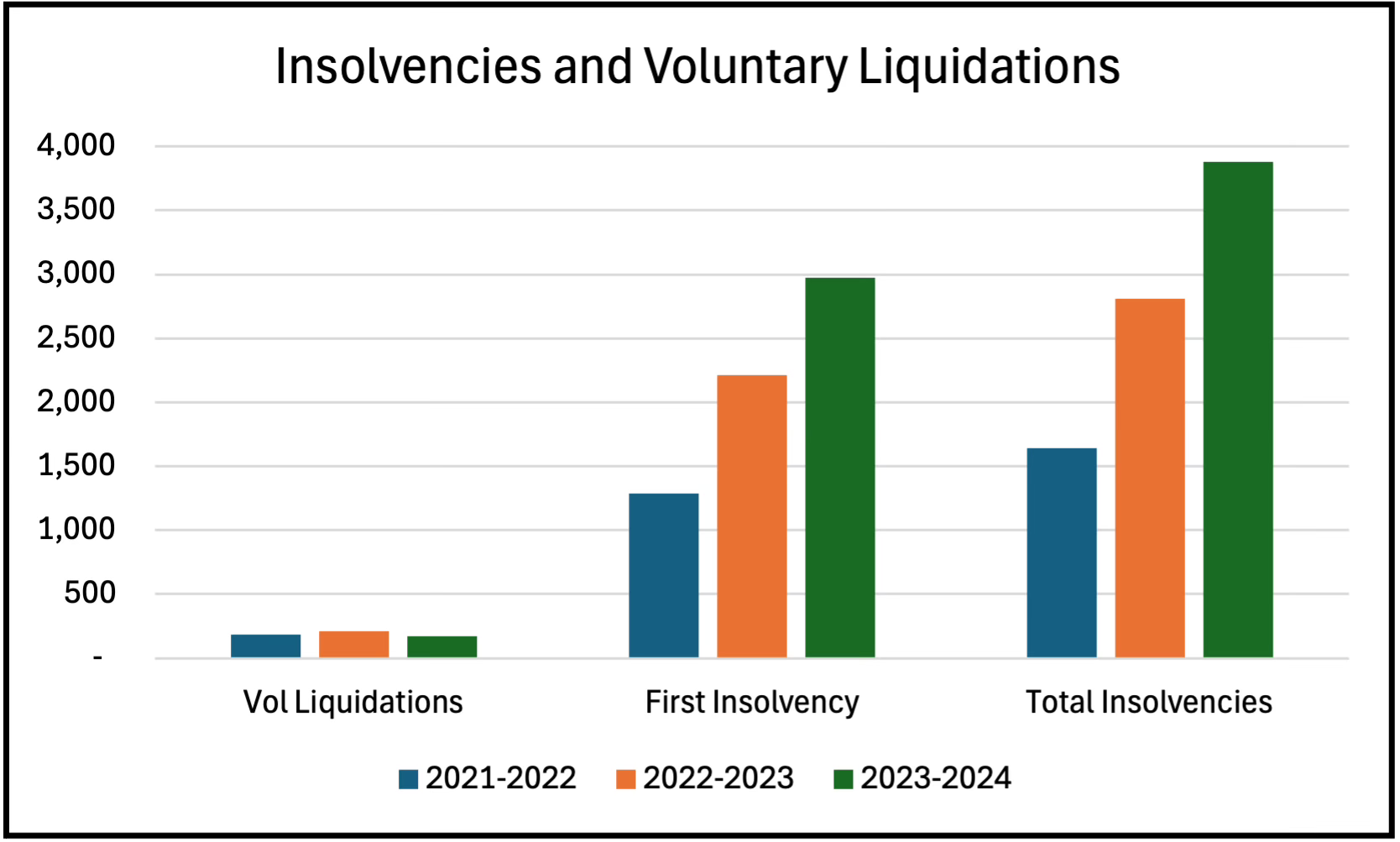

Data on insolvencies comes from the Australian Securities and Investment Commission (ASIC). There are three data sets: insolvencies where an external administrator is appointed for the first time; for any later appointment of an administrator to that business; and for voluntary liquidations where a insolvent business is no longer operating. Figure 1 shows this data for three years to 2024. In those years there were only 185, 213 and 170 voluntary liquidations.

Construction insolvencies where an administrator or controller was appointed for the first time went from 1,284 in 2021-2022, to 2,213 in 2022-2023, then up to 2,977 in 2023-2024. This was a significant increase, and is the number that is typically used in media reports on construction insolvencies (e.g. Australian Financial Review, Macrobusiness).

A better number includes businesses failing for a second time, or more, after a restructuring and agreement with creditors that allowed a business to continue. There were 355, 599 and 905 of these in the three years, so there was a big increase in construction businesses going into administration again in 2023-2024. Adding repeat insolvencies to first insolvencies and voluntary liquidations gives the total for all insolvencies.

Figure 1. Australian construction 2022-2024

Source: ASIC

Construction does have the highest number of insolvencies compared to other industries, but the construction share of total insolvencies has not been increasing, and was 25, 27 and 26 percent in these three years. This is higher than the construction share of the total number of Australian businesses, which is 17 percent, but construction also has a higher proportion of micro and small businesses than other industries.

Two of the reasons why construction businesses are more likely to become insolvent are this prevalence of micro and small firms and the knock-on effects on subcontractors when a contractor goes under, where many of the unsecured creditors will be subcontractors on their projects. Most subcontractors are micro or small businesses, and many are extremely vulnerable to a contractor’s insolvency. Businesses employing less than 5 people account for 65 percent of all construction businesses, and these businesses have little capital and few resources. Micro and small businesses therefore have a much higher insolvency rate than larger businesses.

Because of measures put in place to support industry during the Covid pandemic there were fewer insolvencies than usual in 2021-2022, with a total of 1,639 construction businesses going into administration. The numbers for 2023 and 2024 are more typical, and these show a substantial increase in total insolvencies from 2,812 to 3,882.

However, in June 2024 there were 452,626 operating construction businesses, so the insolvency rate was less than one percent. Further, there are many more businesses in Construction than any other industry. The industry with the second highest number is Professional, Scientific and Technical Services with 344,311 businesses, the third is Rental, Hiring and Real Estate Services with 298,764 businesses, and the fourth is Transport, Postal and Warehousing with 237,326 businesses. This is an important piece of context that should be taken into account when considering insolvencies.

Construction Industry Entry and Exit

How does the number of ASIC insolvencies compare to the ABS Count of Businesses data?

The ABS numbers for annual business exits are much larger than the number of insolvencies, and were 69,972 in 2021-2022, 78,667 in 2022-2023, and 81,354 in 2023-2024. There was a substantial increase between 2022 and 2023 as pandemic measures were unwound, but the increase between 2023 and 2024 was not as great.

Clearly, a few thousand insolvencies a year is not the main driver of exits from the construction industry, and the cumulative total was only 8,333 insolvencies over the three years. There is also some unknown proportion of exits of businesses that have paused operation and stopped paying GST for a couple of years, probably because of market conditions.

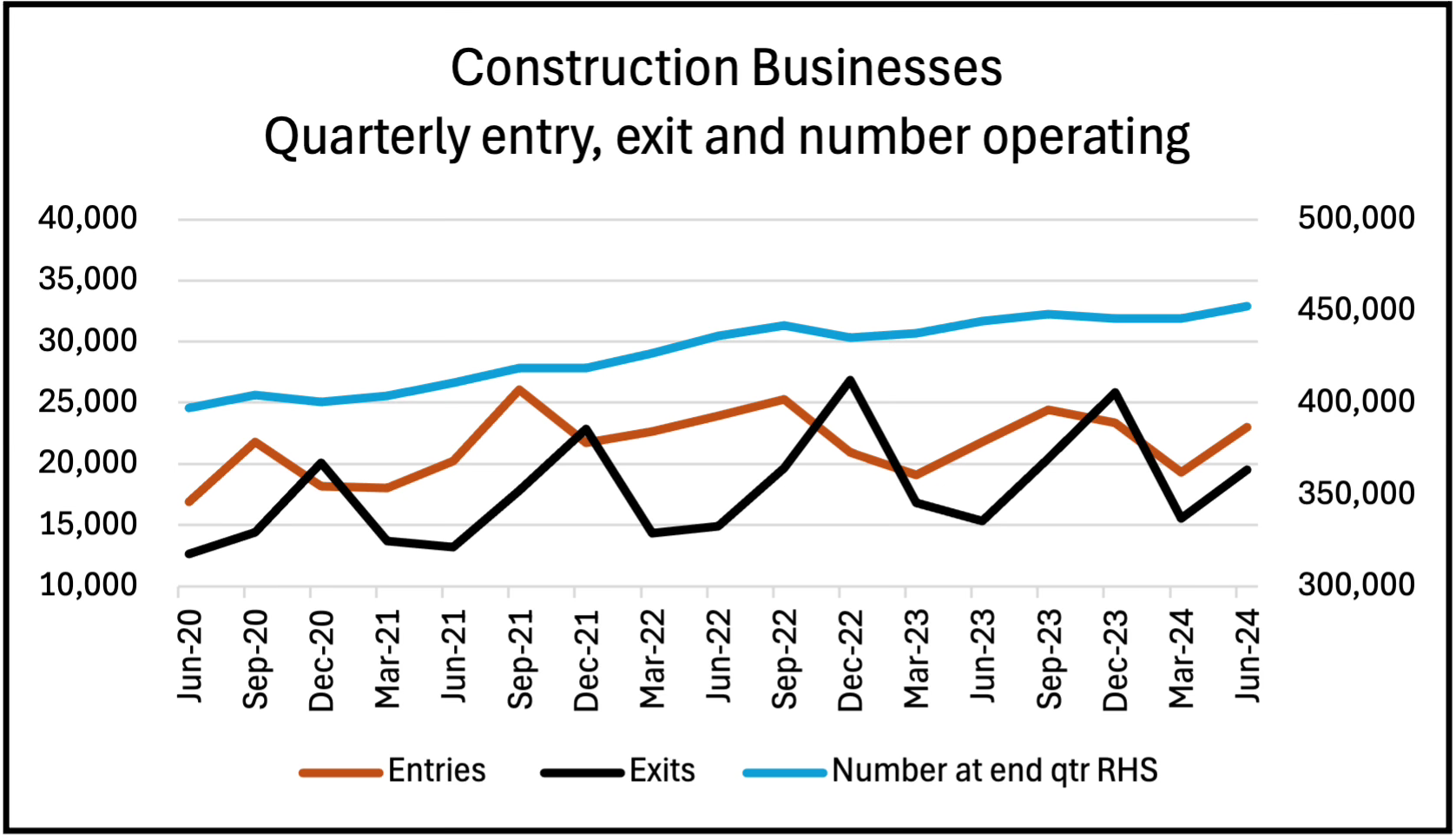

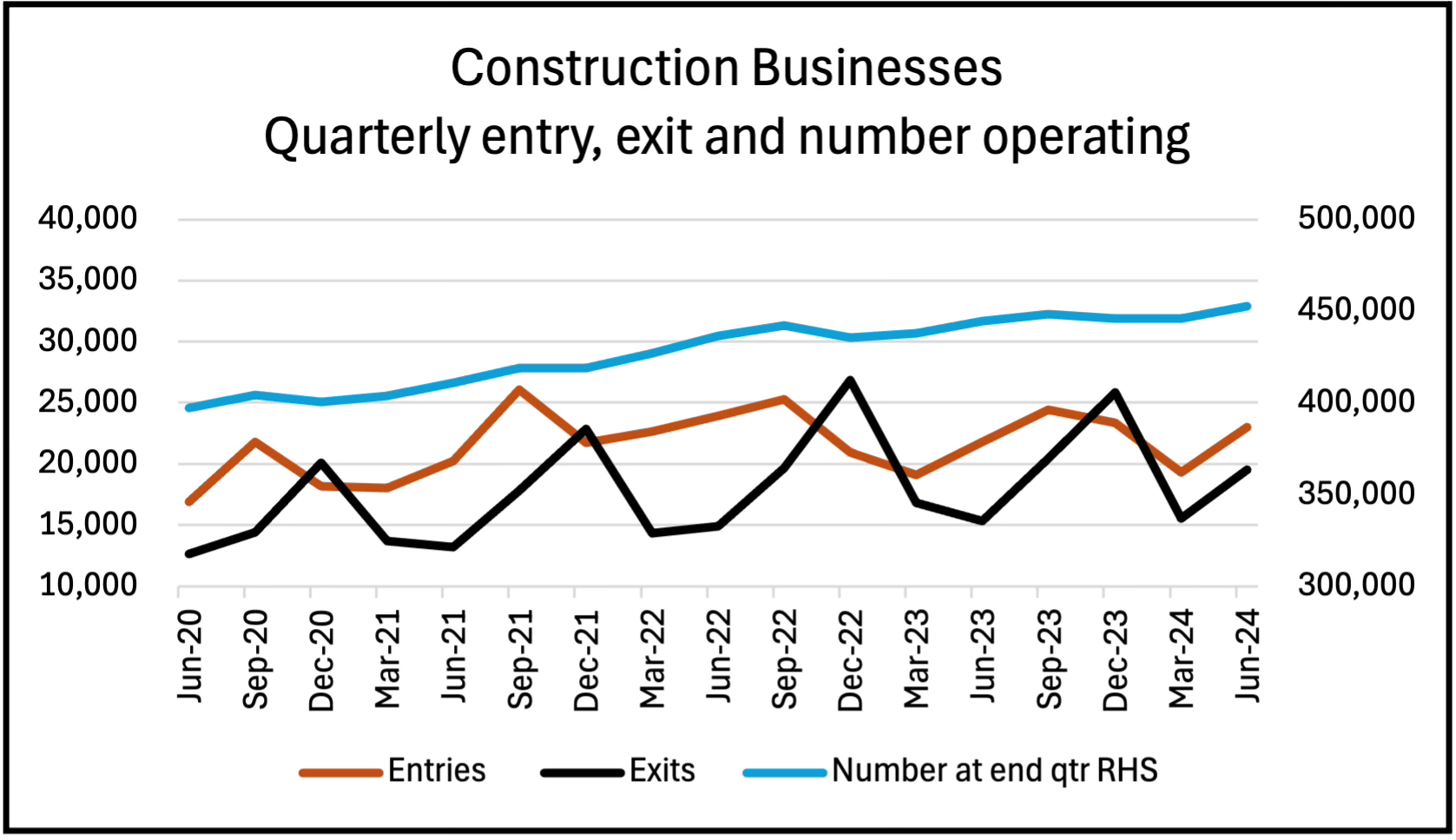

The ABS data is quarterly, and for exits in particular there is a marked seasonal pattern, with a cycle that peaks in the December quarter and has a low in the March or June quarters. As Figure 2 shows, there is a different cycle for entry, which peaks in the September quarter. What is driving these regular cycles of entry and exit is a matter for speculation. Entries can be births (new ABNs) or other (an ABN that has been reclassified or restarted GST payments). For Construction, in most quarters there are more births than others, for example in the June 2024 quarter there were 12,229 births and 10,753 other entries.

There are, over time, more entries than exits, except for the December quarter. The average quarterly number for exits since 2020 was 17,886 and for entries was 21,574. The net result is that the number of construction businesses has been increasing steadily since 2020, rising from 397,920 in June 2020 to 452,626 in June 2024, a 14 percent increase in the number of businesses. If the number of businesses is representative of industry capacity and the supply side of construction, these numbers suggest industry capacity has been increasing.

Figure 2. Australian construction

Source: ABS 8165

The ABS also has overall entry and exits by employment size, although this is not given for individual industries. In 2023-2024 Non-employing businesses had an exit rate of 17.7 percent, and businesses employing 1 to 4 people an exit rate of 9.5 percent. These rates are much higher than those for larger businesses, those employing 5 to 19 people was 5.5 percent, businesses employing 20 to 199 people 3.1 percent, and those employing over 200 had an exit rate of 3.2 percent. As noted above, exit rates are not the same as insolvencies, but this is good evidence of a higher rate of insolvencies in the micro and small businesses that are the great majority of construction firms.

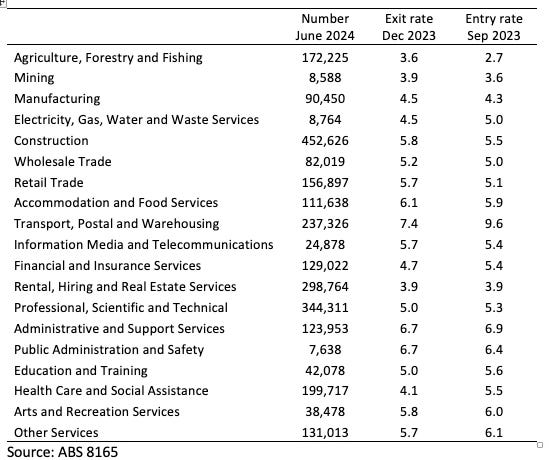

The ABS calculates industry entry and exit rates as percentages, and Construction does not have the highest rates. As Table 1 shows, there are many industries with similar or higher entry and exit rates, although no other industry has a larger number of businesses than Construction. In the 2023 December quarter the exit rate was higher than the 5.8 percent for Construction in five industries, and around the same rate in five others. In the 2023 September quarter the entry rate was higher in six industries, and around the same in seven others. In those quarters for all Australian businesses the exit rate was 5.3 percent and the entry rate was 5.5 percent, so the exit rate for Construction was slightly higher and the entry rate exactly the same.

Table 1. Number of businesses, entry and exit rates in peak months, by industry

Construction Industry Sub-divisions

The ABS also provides data for the three industry sub-divisions. The numbers for operating businesses are of particular interest. In June 2024 there were 10,542 Engineering construction businesses, 108,764 Building construction businesses, and 332,320 Construction services businesses. These sub-divisions had 2.3, 24 and 73.7 percent of the total number of construction businesses.

The same pattern of a December quarter high for exits and a September quarter high for entries also holds for the sub-divisions, with December 2022 having the largest number of exits for all three sub-divisions. The March 2023 quarter was the low for entries for Building construction and Construction services, and March 2024 the low for entries in Engineering construction. Figures 3, 4 and 5 have this data.

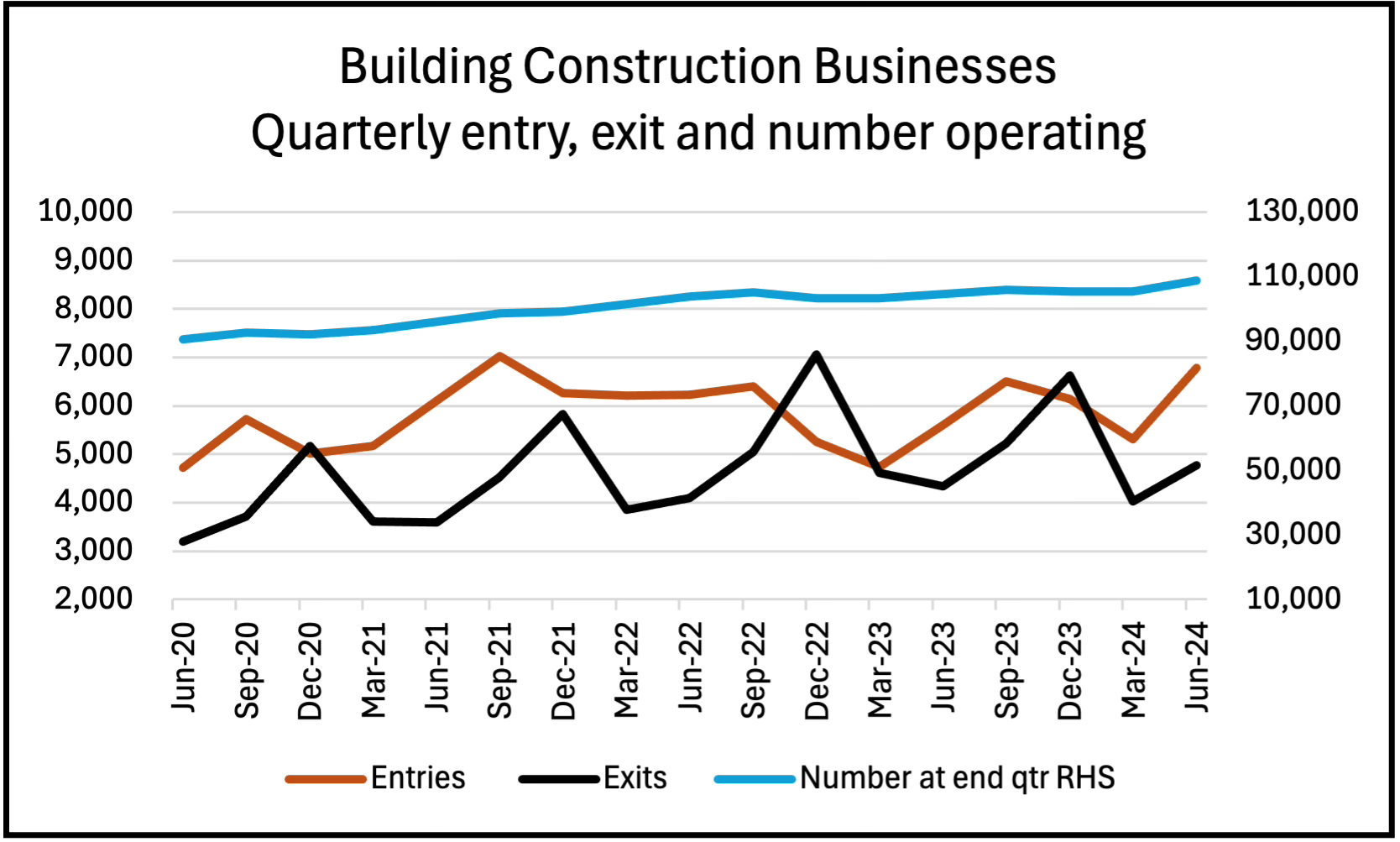

Figure 3. Australian Building construction

Source: ABS 8165

Figure 4. Engineering construction

Source: ABS 8165

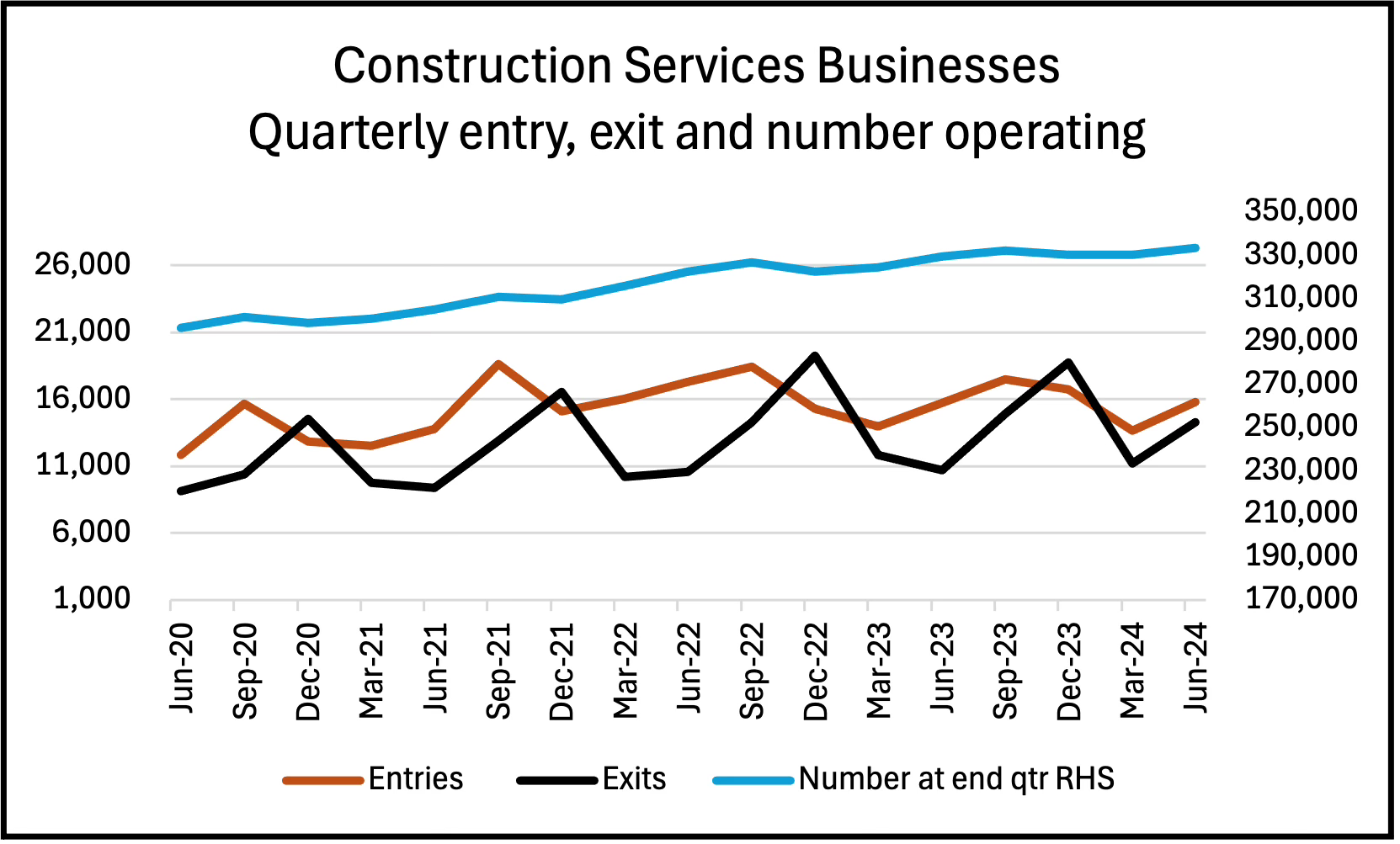

Figure 5. Construction services

Source: ABS 8165

For all three sub-divisions the total number of businesses has been increasing. Between June 2020 and June 2024 the number of Engineering Construction businesses went from 10,052 to 10,542, Building Construction businesses from 90,722 to 108,764, and Construction Services businesses from 296,246 to 332,320. As percentage increases over four years these were 5, 20, and 13 percent respectively. The average quarterly number of exits and entry between 2020 and 2024 for Engineering were 363 and 395 businesses, for Building were 4,666 and 5,837 businesses, and for Construction Services were 12,858 and 15,543 businesses.

Conclusion

ASIC data shows a total of 3,882 construction businesses becoming insolvent in 2023-2024, and it was the industry with the highest number of failures with 26 percent of all insolvencies. However, this needs to be kept in context, because Construction has by far the largest number of businesses compared to other industries and in 2024 had 17 percent of all businesses, and with over 450,000 businesses and a failure rate of less than one percent. It is misleading to claim Construction has an exceptionally high number of insolvencies.

The ABS numbers for annual business exits are much larger than the ASIC number of insolvencies, and were 69,972 in 2021-22, 78,667 in 2022-23, and 81,354 in 2023-24. There was a substantial increase between 2022 and 2023 as pandemic measures were unwound, but the increase between 2023 and 2024 was not as great. Clearly, the insolvency of a few thousand businesses is not the main driver of exits from the construction industry.

The ABS data for exits has a marked seasonal pattern, with a cycle that peaks in the December quarter and a low in the March or June quarters. There is a different cycle for entry, which peaks in the September quarter. What is driving these regular cycles of entry and exit in Construction is a matter for speculation.

Many industries have higher entry and exit rates than Construction, although no other industry has a larger number of businesses. In the 2023 December quarter the exit rate in five industries was higher than in Construction and around the same rate in five others. In the 2023 September quarter the entry rate was higher in six industries, and around the same in seven others.

There are more entries than exits, except for the December quarter. The average quarterly number for exits since 2020 was 17,886 and for entries was 21,574, so the number of construction businesses has been increasing steadily since 2020, rising from 397,920 in June 2020 to 452,626 in June 2024, a 14 percent increase in the number of businesses. If the number of businesses is representative of industry capacity and the supply side of Construction, these numbers suggest industry capacity has been increasing.

For all three sub-divisions the number of businesses has been increasing. Between June 2020 and June 2024 the number of Engineering Construction businesses went from 10,052 to 10,542, Building Construction businesses from 90,722 to 108,764, and Construction Services businesses from 296,246 to 332,320. These sub-divisions had 2.3, 24 and 73.7 percent of the total number of construction businesses, and their percentage increases over four years were 5, 20, and 13 percent respectively.

Construction businesses are more likely to exit or become insolvent because two thirds are micro or small businesses employing less than 5 people, which have a higher rate of insolvency than larger businesses. Subcontractors are also vulnerable to the knock-on effects on their capital and cash flow of a contractor’s insolvency, where many of the unsecured creditors will be subcontractors. Although exit rates are not the same as insolvencies, the ABS data is good evidence of a much higher rate of insolvencies in the micro and small businesses that are the great majority of construction firms. This is an important piece of context that should be taken into account when considering insolvencies.